You may be torn between buying a home now or waiting. But don’t forget to factor in the equity you’ll gain as prices rise.

Experts forecast prices will climb over the next 5 years – and based on those forecasts, you could gain about $90k in equity in that time.

So, you could wait, but you’ll miss out on a lot of equity if you do. If you’re ready and able to buy, let’s connect so you can start growing your wealth now.

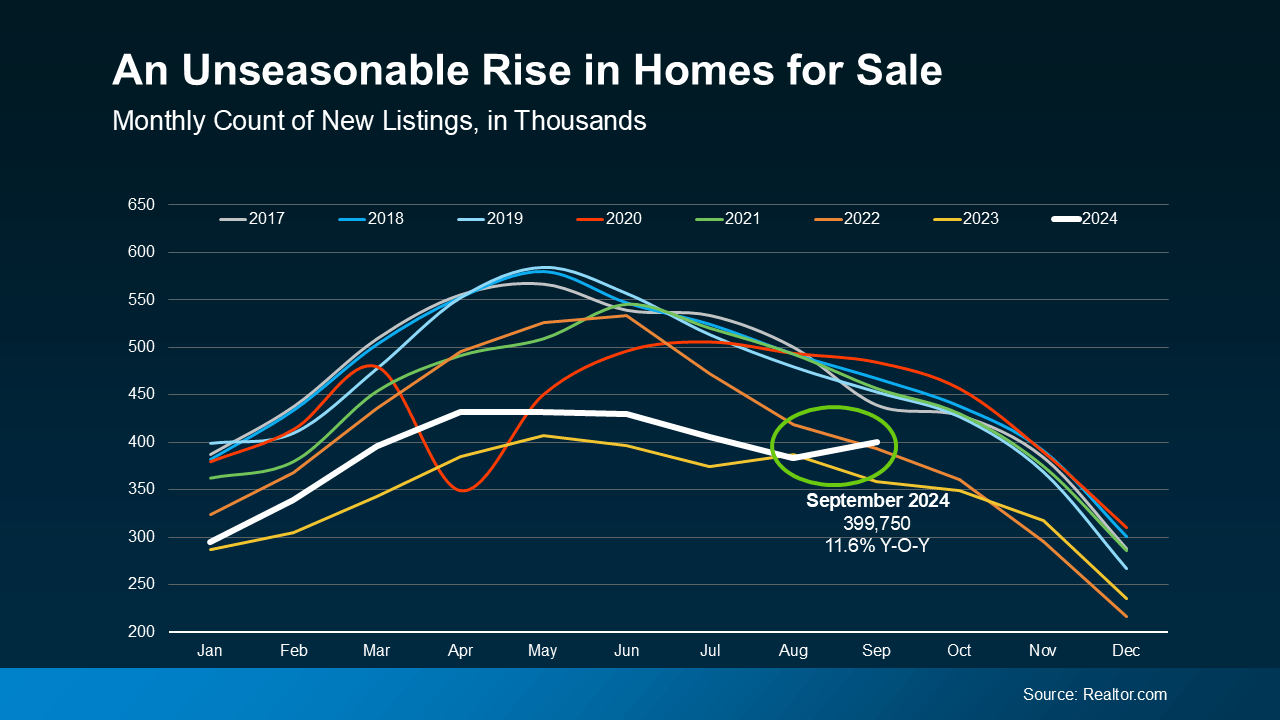

Why Did More People Decide To Sell Their Homes Recently?

Homeowners typically slow down their moving plans as the summer months wrap up, and as a result, fewer homes are listed for sale in the fall. It’s a predictable, seasonal trend in real estate. But this year, mortgage rates came down at the same time the number of homes on the market usually starts to decline. So, what happened? More homeowners decided to sell, so more homes came to the market.

The most recent data from Realtor.com reveals that in September, the number of homes put up for sale increased by 11.6% compared to this time last year.

As the green circle in the graph below shows, the typical September decline in homes coming to the market didn’t happen – that number actually went up (see graph below):

Ralph McLaughlin, Senior Economist at Realtor.com, explains why there was an unseasonable rise:

“This sharp increase is largely due to the decline in mortgage rates in mid-August, enticing homeowners to sell.”

So, as rates came down at the end of the summer, more people jumped into the market and decided to make their move.

What Does This Mean If You’re Looking To Buy a Home?

It means morefresh options to choose from than you’ve had in a while – not the ones that have been sitting around, unsold.

But keep in mind, mortgage rates have been volatile lately, ticking up slightly in recent weeks, which could limit the number of people who feel comfortable with the idea of selling in the months ahead. And in this market, it’s mortgage rates that are largely driving homeowner decisions.

Why Buy Now, Rather Than Wait?

Whether you’re looking for a starter home, an upgrade, or hoping to downsize, you have more homes to choose from right now. And if you can find what you’re looking for, know that these new, fresh options won’t be on the market forever. So, staying on top of what’s available in your local area with a trusted agent is key.

And remember, one month doesn’t make a trend. So, what does that mean going forward? Whether more homeowners than normal continue to put their houses on the market will largely depend on what happens with mortgage rates and the economic factors that impact them, like inflation, employment, and the reactions by the Federal Reserve.

With that in mind, now might be your moment, while more homes are available – if you’re ready, willing, and able to buy this fall.

Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), explains:

“The rise in inventory – and, more technically, the accompanying months’ supply – implies home buyers are in a much-improved position to find the right home and at more favorable prices.”

Bottom Line

As rates came down at the end of the summer, sellers started to trickle back into the market, which means buyers have more choices right now. Let’s connect to make sure you have a trusted advisor to help you navigate the new options before they’re all scooped up.

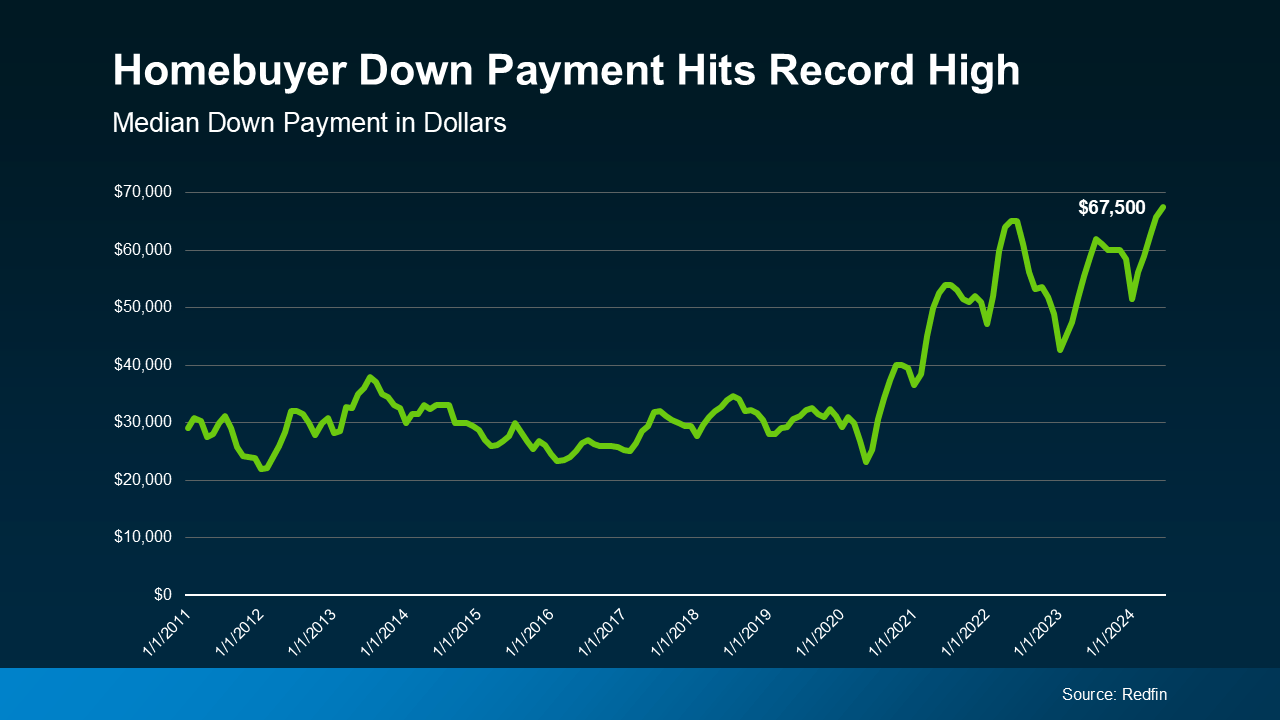

The Benefits of Using Your Equity To Make a Bigger Down Payment

Did you know? Homeowners are often able to put more money down when they buy their next home. That’s because, once they sell, they can use the equity they have in their current house toward their next down payment. And it’s why as home equity reaches a new height, the median down payment has too.

According to the latest data from Redfin, the typical down payment for U.S. homebuyers is $67,500—that’s nearly 15% more than last year, and the highest on record (see graph below):

Here’s why equity makes this possible. Over the past five years, home prices have increased significantly, which has led to a big boost in equity for current homeowners like you. When you sell your house and move, you can take the equity that gives you and apply it toward a larger down payment on your new home. That’s a major opportunity, especially if you’ve had concerns about affordability.

Now, it’s important to remember you don’t have to make a big down payment to buy your next home—there are loan programs that let you put as little as 3%, or even 0% down. But there’s a reason so many current homeowners are opting to put more money down. That’s because it comes with some serious perks.

Why a Bigger Down Payment Can Be a Game Changer

1. You’ll Borrow Less and Save More in the Long Run

When you use your equity to make a bigger down payment on your next home, you won’t have to borrow as much. And the less you borrow, the less you’ll pay in interest over the life of your loan. That’s money saved in your pocket for years to come.

2. You Could Get a Lower Mortgage Rate

Providing a larger down payment shows your lender you’re more financially stable and not a large credit risk. The more confident your lender is in your credit score and your ability to pay your loan, the lower the mortgage rate they’ll likely be willing to give you. And that amplifies your savings.

3. Your Monthly Payments Could Be Lower

A bigger down payment doesn’t just help you reduce how much you have to borrow—it also means your monthly mortgage payment may be smaller. That can make your next home more affordable and give you a bit more breathing room in your budget.

4. You Can Skip Private Mortgage Insurance (PMI)

If you can put down 20% or more, you can avoid Private Mortgage Insurance (PMI), which is an added cost many buyers have to pay if their down payment isn’t as large. Freddie Mac explains it like this:

“For homeowners who put less than 20% down, Private Mortgage Insurance or PMI is an added insurance policy for homeowners that protects the lender if you are unable to pay your mortgage. It is not the same thing as homeowner’s insurance. It’s a monthly fee, rolled into your mortgage payment, that’s required if you make a down payment less than 20%.”

Avoiding PMI means you’ll have one less expense to worry about each month, which is a nice bonus.

Bottom Line

Down payments are at a record high, largely because recent equity gains are putting homeowners in a position to put more money down.

If you’re thinking about selling your current house and moving, let’s work together to figure out how much home equity you have right now, and how it can boost your buying power in today’s market.

Why an Agent Is Essential When Buying a Newly Built Home

For some buyers, there’s a misconception that newly built homes aren’t made to last or fall short of the quality you can find in older homes. Unfortunately, this is turning some buyers away from what may be one of their best options in today’s housing market. As Builder Online says:

“As resale inventory remains limited and the price spread between new and resale homes narrows, new homes are increasingly an attractive value proposition for buyers, with incentives such as rate buydowns a way to help address ongoing affordability challenges.”

So, is there any merit to the myth? Let’s break down the best way to make sure you feel good about looking into new home construction. That way, you’re not missing out on such a great option today.

Choosing the Right Builder

The key to making sure you get a quality newly built home is to choose a good builder. Reputable builders adhere to strict building codes and standards, use advanced construction techniques, and often offer warranties that cover structural issues for several years. That’s why the Mortgage Reports offers this advice:

“When embarking on the journey of buying a new construction home, one of the most important steps is selecting the right builder. This decision can significantly impact the quality and satisfaction you derive from your new home.”

And while you could dig into research about all the builders in your area, there’s an easier option to get the job done: lean on a pro. When you work with a local real estate agent, they already know about the builders and the new home communities under construction in your area.

Beyond that, maybe they’ve even worked with other buyers who opted for a home in one of those neighborhoods. Here are just a few of the things your agent will help you with:

1. The Builder’s Reputation: Your agent will help point you toward builders with strong reputations and positive reviews from previous buyers. Additionally, your agent will make sure the builder is licensed and insured. Membership in professional organizations, such as the National Association of Home Builders (NAHB), is also a good sign of a builder’s commitment to industry standards.

2. Their Model Homes: Your agent will also be able to tell you if the builders have model homes you can tour. And when your agent walks through the model with you, they’ll draw your attention to the little details that matter most. Things like the quality of finishes, layout, and overall feel of the home.

3. Builder Warranties: Your agent will also be able to help you navigate any builder offers or incentives. Reputable builders often provide warranties to cover major structural elements of the home for a significant period of time. This is a testament to their confidence in the quality of their construction.

4. Getting Inspections: Even with new homes, inspections are crucial. Your agent will coordinate the inspections with licensed professionals to ensure the home meets safety and quality standards before you move in.

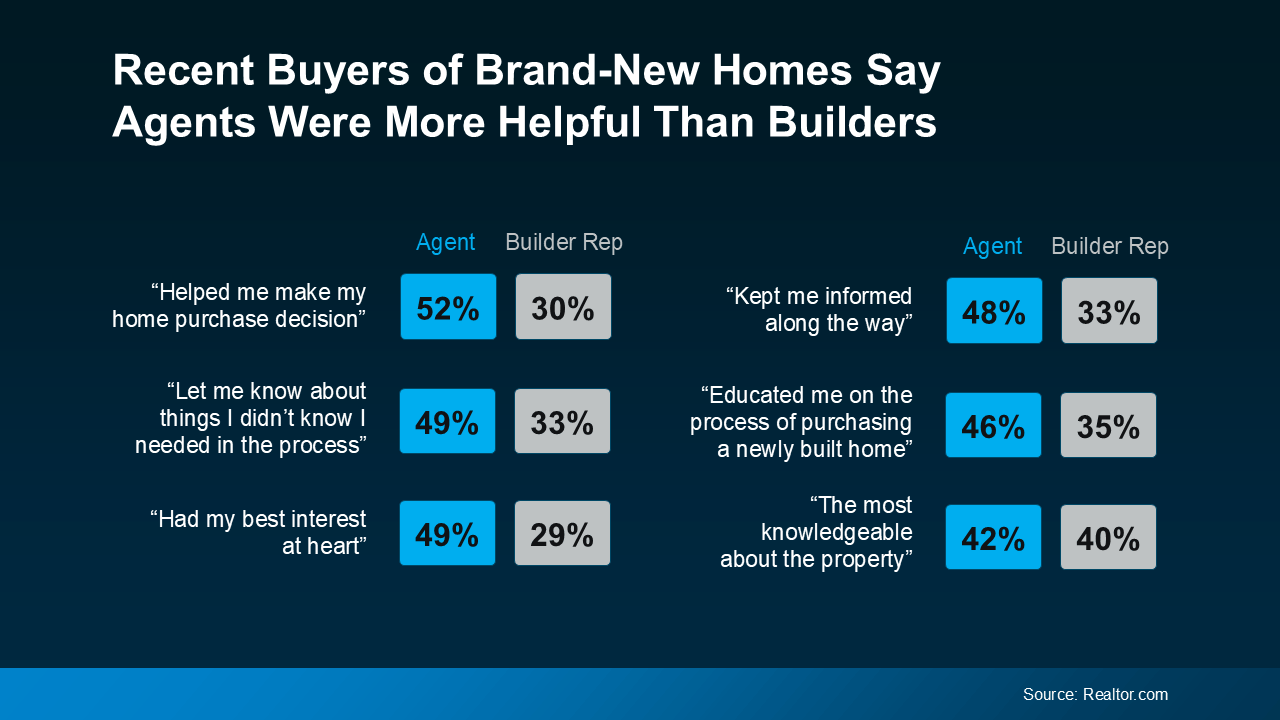

Agents Are the MVP When You’re Buying a Brand-New Home

Maybe that’s why data shows homebuyers unanimously scored their agents higher than their builders when looking back on their recent purchase:

So, you don’t need to worry that they just don’t make them like they used to. By working with a knowledgeable real estate agent to choose a reputable builder, you can feel confident when buying a newly built home today. As Realtor.comsays:

“If you are interested in buying a new construction . . . You need your own real estate agent from the get-go. Even if it seems like plug and play to sign up with the builder’s on-site agent, you’re going to want someone representing your side of the deal.”

Bottom Line

If you’re considering buying a brand-new home, don’t let misconceptions hold you back. Let’s work together to find a home you’ll love and be proud to call your own.

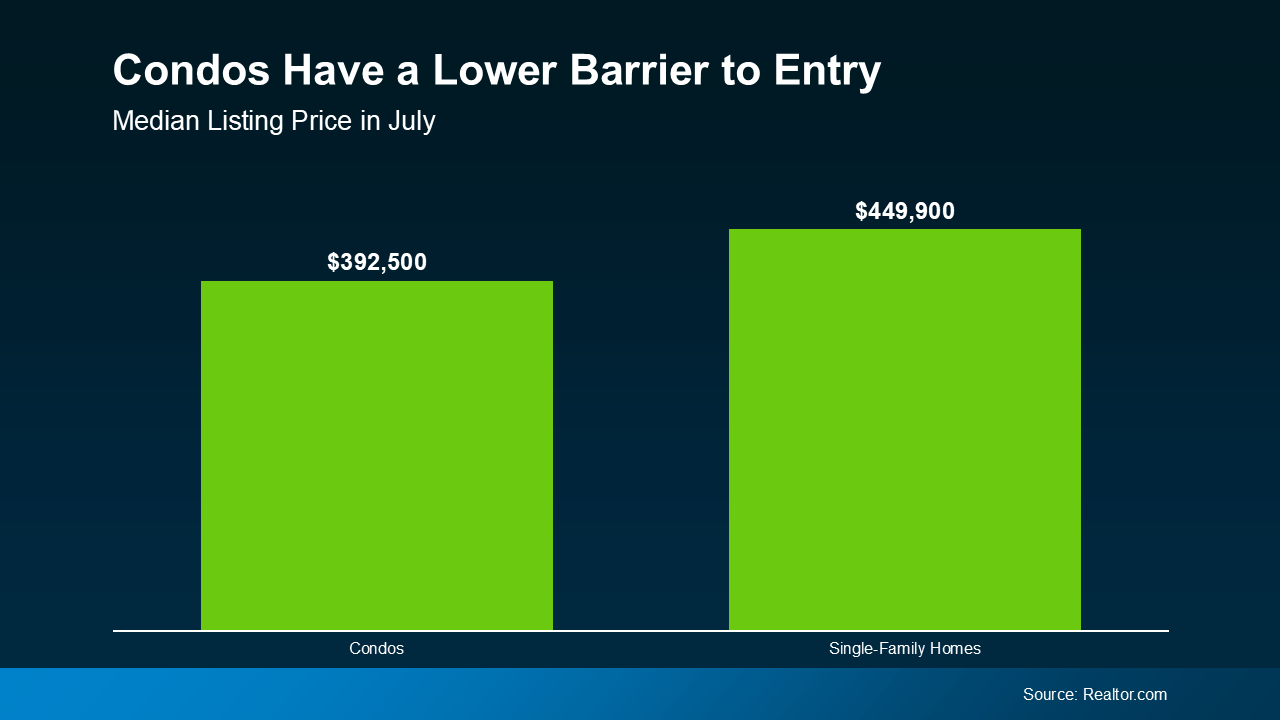

If you’re looking to break into homeownership but the price of single-family homes has you second-guessing, you might want to consider a condominium (condo) or townhome. These types of homes often come with a lower barrier to entry – and that can help you start to build equity and enjoy the benefits of owning a home sooner.

Since they’re usually smaller than single-family homes, they can be easier on your wallet. While it’s not always the case, smaller square footage usually comes with a smaller price tag too. As a result, according to the latest data from Realtor.com, condos typically have a lower asking price than single-family homes (see graph below):

And here’s some exciting news: builders are focusing more on homes like these. The National Association of Home Builders (NAHB) says:

“The share of townhomes being built is at an all-time high.”

That means there’s a good number of options to add to your home search if you broaden it to include condos and townhomes. And you may even find something that works better for your budget.

So, if you’re comfortable with a smaller space and want to buy your first home before the spring rush, adding these types of homes to your search might be your answer.

The Perks of a Condo Lifestyle

Living in a condo has a bunch of other perks, too. Let’s look closer at why condos are appealing for first-time buyers:

They help you start building equity. When you buy a condo or townhome, you build equity and your net worth as you make your mortgage payments and as your condo’s value goes up over time.

They can be low maintenance. Condos are great if you want to own your place but don’t want to mow the lawn, shovel snow, or fix the roof. Your real estate agent can help explain any associated fees and details for the condos you’re interested in.

They usually come with a range of amenities. Your condo might come with access to a pool, dog park, or parking. And the best part? You don’t have to take care of any of them.

They create a sense of community. Buying a condo means you’ll be living close to other people, which is nice if you want a more close-knit feel. Many communities like these hold fun events such as barbecues and parties to help create that sense of connection among residents.

Remember, your first home doesn’t have to be the one you stay in forever. The important thing is to get your foot in the door as a homeowner so you can start to gain home equity. Later on, that equity can help you buy another place if you want something different.

Ultimately, owning and living in a condo or townhome is a lifestyle choice. If you want to see if it makes sense for you, talk to a local real estate agent.

Bottom Line

Ready to find a home that suits your goals? A condo might be the perfect fit for your first home purchase. Let’s connect today to start your search.

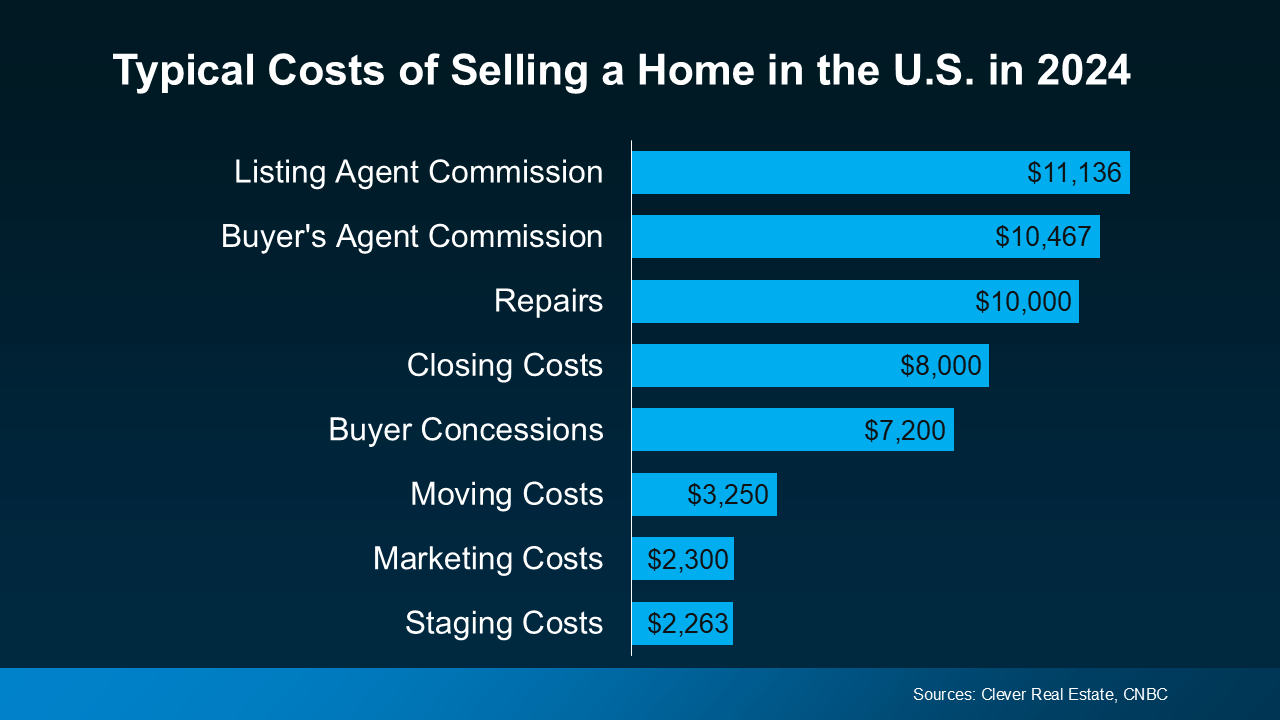

If you’re toying with the idea of selling your house, you’re probably wondering how much it’ll cost. To be honest, the final number will depend on several factors like the offer you accept, if you help with your buyer’s closing costs, how many repairs you tackle, and more.

So, to give you a ballpark of what to expect, here’s some information on a few of the expenses you’ll want to be ready for (see graph below):

But here’s something that puts those costs into perspective. Most homeowners today have a substantial amount of equity built up in their homes, and that means they stand to make significant gains when they sell. Chances are, you do too. This can help quickly recoup these selling costs. You may even have enough equity leftover to put some toward your next home purchase too.

Let’s dive into a few of the costs from the graph above, so you have a bit more context on what they include and where you may be able to save some money, when it makes sense.

Closing Costs and Commission

These are the fees you’ll pay at the closing table to cover various aspects of the sale. You’ll have your own closing costs and you may even offer to pay some of the buyer’s as a concession. As U.S. News Real Estate explains:

“Closing costs are fees that are paid to finalize the transaction and transfer ownership of the home to the buyer . . . Sellers can expect to pay 2% to 4% of the sale price of the home in fees and taxes on top of the agent commission. Based on the national median home sale price, this means that closing costs in 2023 for sellers are about $7,740 to $15,480. . .”

Taxes are going to vary by state and agent commissions depend on what you agree upon upfront. And keep in mind, that the numbers in the chart above are just an example, not exact figures. Not to mention, if you put money toward things like your property taxes, mortgage escrow, etc. as part of your current mortgage payments – there’s a chance you’ll get a credit back at closing that can help offset some of these selling expenses.

Pre-Listing Inspection and Repairs

One optional step some sellers take is having a pre-listing inspection. It gives you an idea of what may pop up later on in the buyer’s inspection – because those are the items a buyer may ask you to toss in a credit (or concession) to cover later on.

This allows you to get a jump on any repairs and tackle them before you list, so your house is set up to impress from the start.

Again, if you want to skip this step, an agent can help. They’ll be able to give you advice on things like paint colors, small cosmetic repairs, what buyers are looking for, and whether it’s worth tackling anything else ahead of time. This will help make sure you’re spending money on things that are most likely to net you a solid return on your investment.

Home Staging

As inventory grows, you may want to take a few extra steps to make sure your house stands out. Staging is an optional way to make sure your house shows well. It can include bringing in rental furniture if the house is vacant or art to warm up the walls. Some staging can even be done virtually once the photos are taken. But, in general, how much does it cost? According to Bankrate:

“Home sellers typically pay somewhere between $782 and $2,817 in home staging costs . . . but the price tag can vary widely.”

If you want to skip this step, you could opt to lean on your agent’s advice for what looks good and what may feel cluttered. A great agent will suggest things like removing a chair to open up the flow of a room, laying down a rug to add warmth to a space, or taking down photographs to de-personalize strategic areas.

Why Leaning on an Agent Is Key

If you’re looking to cut down on your costs, you have options. But be careful of where you trim. You may be able to skip staging or a pre-listing inspection since those are optional, but you don’t want to skimp and sell without a pro.

An agent is your go-to expert throughout the transaction. They’ll offer customized advice every step of the way, including how to stage the house and what repairs to tackle. This can help you avoid hiring an outside stager or having to pay for a pre-listing inspection.

But that’s not the only way your agent adds value. They’ll also create tailored marketing and pricing strategies that’ll highlight the house’s best assets and any work you did to get the home show ready. And that can actually help your house sell for more in the long run.

Bottom Line

Want a better picture of what you should expect when you sell your house? Let’s have a conversation and walk through it together.

You may have heard chatter recently about the economy and talk about a possible recession. It’s no surprise that kind of noise gets some people worried about a housing market crash. Maybe you’re one of them. But here’s the good news – there’s no need to panic. The housing market is not set up for a crash right now.

“A housing market crash happens when home values plummet due to a lack of demand for homes or an oversupply.”

With that definition in mind, here are two reasons why this just isn’t on the horizon.

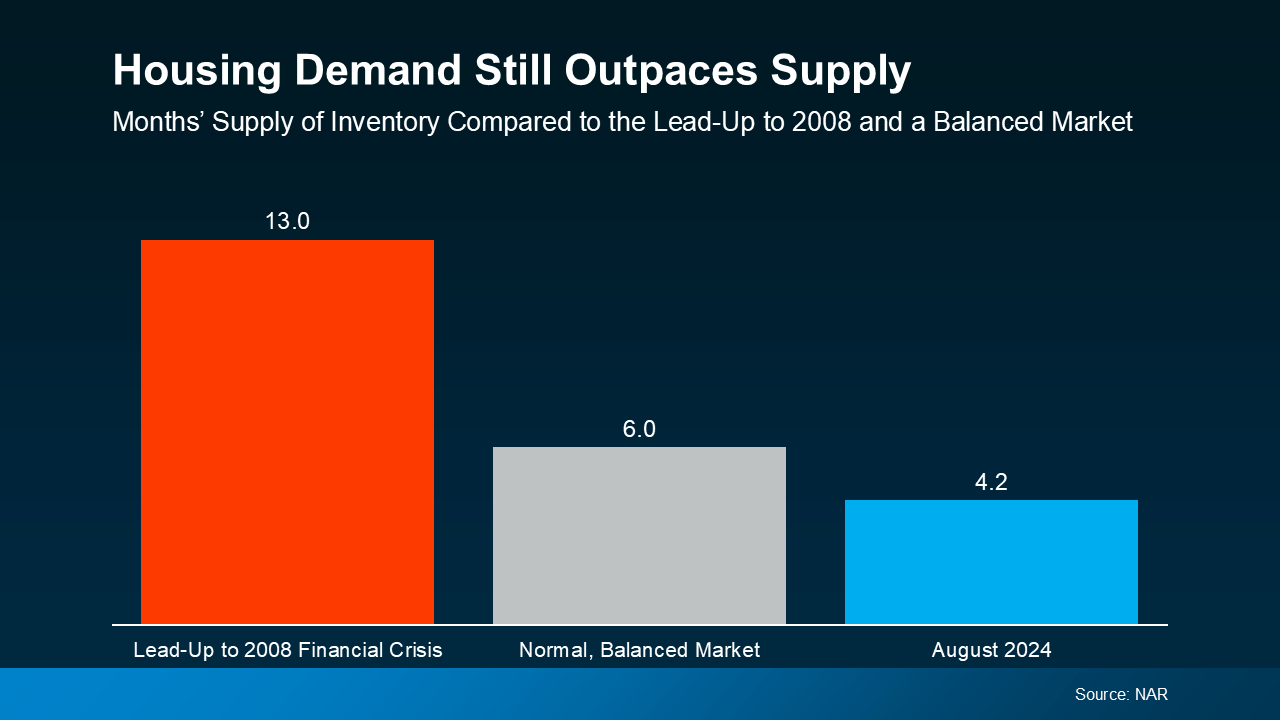

1. Demand for Homes Is Higher than Supply

One of the biggest reasons the housing market crashed back in 2008 was an oversupply of homes. Today, though, it’s a very different story.

It’s a general rule of thumb that a market where supply and demand are balanced has a six-month supply of homes. A higher number means supply outpaces demand, and a lower number means demand outpaces supply. The graph below uses data from NAR to put today’s situation into context:

The graph compares housing supply during three different periods of time. The red bar shows there were 13 months of supply before the 2008 crisis, which was far too much. The gray bar shows a balanced market with six months of supply, for context. And the blue bar shows there are only 4.2 months of supply today.

Put simply, there are more people who want to buy homes than there are homes available to buy right now. So, demand is greater than supply. When that happens, home prices stay steady or rise – the opposite of a housing market crash.

It’s important to note that inventory levels differ from market to market. Some areas may be more balanced, while a few could have a slight oversupply, which can impact prices locally. However, most markets continue to experience a shortage of homes.

Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), says:

“We simply don’t have enough inventory. Will some markets see a price decline? Yes. [But] with the supply not being there, the repeat of a 30 percent price decline is highly, highly unlikely.”

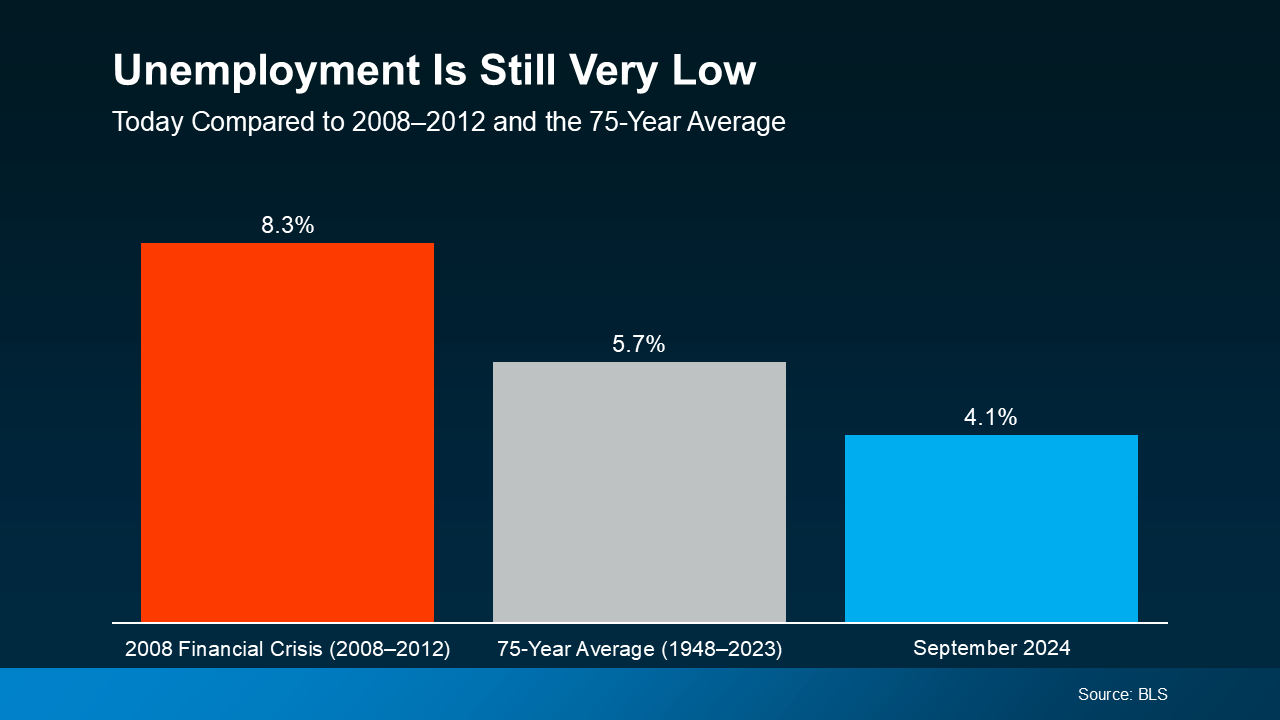

2. Unemployment Is Still Low

When people are unemployed, they’re more likely to have trouble making their mortgage payments and may be forced to sell or face foreclosure. That was a big problem during the 2008 financial crisis. Today, the employment situation is much more stable (see graph below):

Again, this graph shows three different periods of time, but this one is the unemployment rate. The red bar represents the 2008 financial crisis when unemployment was very high at 8.3%. The gray bar shows the 75-year average of 5.7%. And the blue bar shows the unemployment rate today, and it’s much lower at just 4.1%.

Right now, people are working, earning an income, and making their mortgage payments. That’s one reason why the wave of foreclosures that happened in 2008 isn’t going to happen again this time. Plus, since so many people are employed right now, many are actually in a position to buy a home, and this demand keeps upward pressure on prices.

Today’s Housing Market Is Stronger than in 2008

While it’s understandable to be concerned when you hear talk of a recession and economic uncertainty, but know this: the housing market is in a much better place than it was in 2008. According to Rick Sharga, Founder and CEO at CJ Patrick Company:

“Literally everything is different about today’s housing market dynamics than the conditions that led to the housing crisis.”

Demand for homes still outpaces supply, and unemployment remains low. And these are two key factors that will help prevent the housing market from crashing any time soon.

Bottom Line

The housing market is doing a lot better than it was in 2008, but it’s important to remember that real estate is very local.

So, it’s always a good idea to stay informed about our specific market. If you have any questions or want to discuss how these factors are playing out in our area, feel free to reach out.

Why Now’s Not the Time To Take Your House Off the Market

Has your house been sitting on the market longer than expected? If so, you’re bound to be frustrated by now. Maybe you’re even thinking it’s time to pull the listing and wait to see what 2025 brings. But what you may not realize is, the decision to hold off could actually cost you. Here’s a look at why staying the course could be the smarter move.

Other Sellers Are Pulling Back. Should You Hold Off Too?

According to recent data from Altos Research, the number of withdrawals is increasing – that means more sellers are opting to pull their listings off the market right now. And this isn’t unusual for this time of the year.

In the housing market, there are seasonal ebbs and flows. Inventory levels typically start to drop off a bit headed into the fall season as some sellers delay their plans until the new year. As Mike Simonsen, Founder of Altos Research, explains:

“. . . we’re seeing a more normal seasonal pattern now with inventory beginning to decline. We’re also seeing more home sellers withdrawing their listings to try again next year. In fact, for every two sales, there is another listing withdrawn from the market.”

But is that a smart move? While it might seem like a good idea to pull your listing too, here’s why that approach may not pay off this year.

Today’s Buyers Are Serious and Ready To Act

The biggest reason to stick with your plan to sell now is that the buyers who are looking at this time of year are serious about making a purchase.

They’ve been sitting on the sidelines for a while waiting for affordability to improve. And now that mortgage rates are down from their recent peak, they’re ready to make their move. Mortgage applications are rising – and that’s a leading indicator that buyers are preparing to jump back in. And since they’ve already put their needs on the back burner for so long, they’re even more eager than buyers usually are at this time of year.

These aren’t window shoppers. They’re highly motivated buyers who want to move fast – and that’s the kind of buyer you want to work with. As Freddie Macsays:

“During the fall months, serious homebuyers are eager to settle in to a new home before the holiday season ramps up and the winter weather begins.”

By keeping your home on the market, you increase the chances of attracting people who are truly ready to make a purchase.

Bottom Line

While some sellers are choosing to take their homes off the market, this really isn’t the best move. With serious buyers eager to purchase, this is a great time to sell your house. Let’s connect to make sure we’ve got a strategy in place to make it happen.

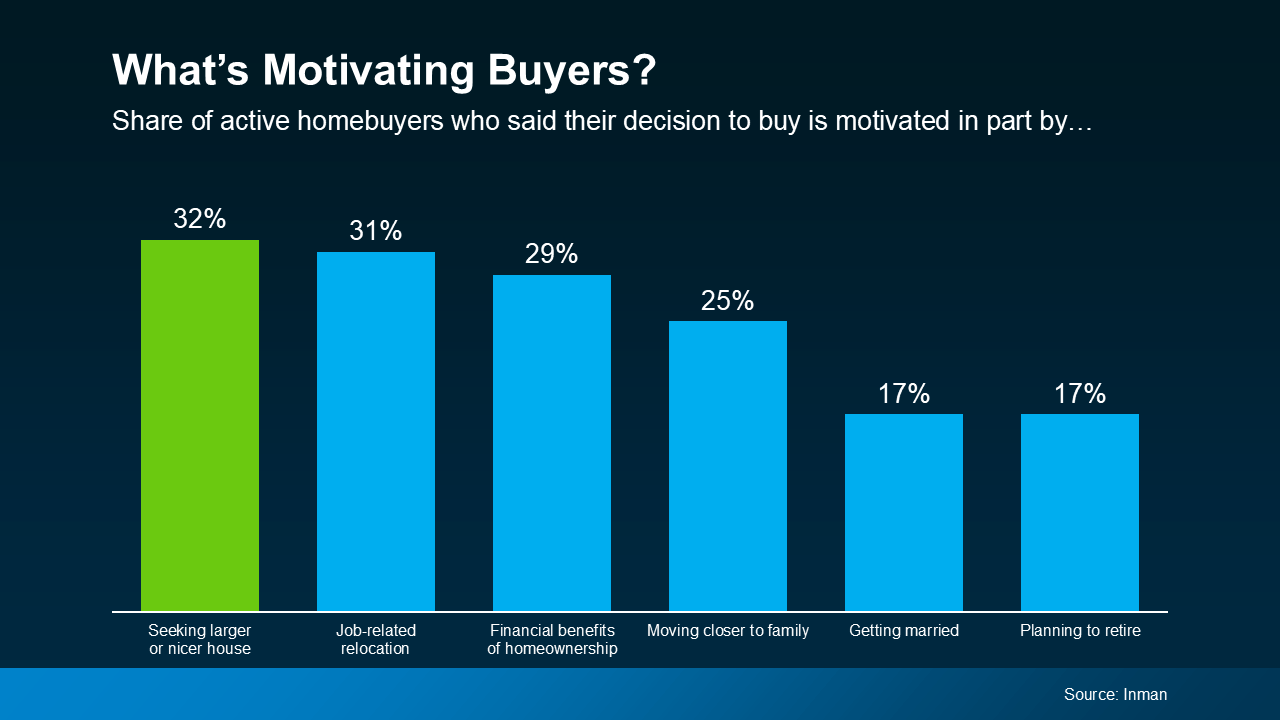

If you’ve been wanting to sell your house and move up to a bigger or nicer home, you’re not alone. A recent Inmansurvey reveals the top motivator for today’s homebuyers is the desire for more space or an upgraded home (see graph below):

But there’s also a good chance you, like many other people, have been holding off on that goal because of recent market challenges. It makes sense – when you’re planning an upgrade that could increase your monthly housing costs, affordability has a huge impact on when you make your move. But there’s good news: now’s actually a great time to make that move happen. Here’s why.

You Have a Lot of Equity To Leverage

One of the key benefits in today’s market is the amount of equity you’ve likely built up in your current house over the years. Even with recent shifts in the housing market, national home prices have steadily grown, adding to the equity homeowners have today. Selma Hepp, Chief Economist at CoreLogic, explains it well:

“Persistent home price growth has continued to fuel home equity gains for existinghomeowners who now average about $315,000 in equity and almost $129,000 more than at the onset of the pandemic.”

What does that mean for you? If you’ve been in your home for a few years, you’re probably sitting on a significant amount of equity. You can put that toward the down payment on your next home, helping keep the amount you borrow within a comfortable range.

This can make upgrading more achievable than you might think. If you’re curious how much you’ve built up over the years, ask your real estate agent for a professional equity assessment.

Mortgage Rates Have Fallen, Boosting Your Purchasing Power

And there’s another big reason why now’s a great time to make your move: mortgage rates are trending down. Lower rates can help make your future monthly payments more manageable, and they also increase your purchasing power. As Nadia Evangelou, Senior Economist and Director of Real Estate Research at the National Association of Realtors (NAR), points out:

“When mortgage rates fall, the interest portion of monthly payments decreases, which lowers the total payment. This makes it easier for more borrowers to . . . qualify for mortgages that may have been unaffordable at higher rates.”

That gives you more flexibility when shopping for homes and may allow you to afford a house at a price point that was previously out of reach. A trusted lender can work with you to figure out the best plan for your budget.

Bottom Line

If you’re ready to sell your current home and find the bigger, nicer home you’ve been dreaming of, don’t wait. Your equity, paired with lower mortgage rates, puts you in a great position to make that move today.

To make the best decisions and get the most out of your current market advantage, let’s connect so you have an expert guide through every step of the homebuying process.

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link