Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Buyer Advice and Aid •

November 13, 2025

Waiting for Rates to Fall Below 6% May Save you Only $80 a Month

Myths About Housing •

November 12, 2025

Are Builders Overbuilding Again? Let’s Look at the Facts.

Are Builders Overbuilding Again? Let’s Look at the Facts.

If it feels like you’re seeing new construction signs pop up everywhere, you’re not wrong. Builders have been busy. And it’s left some people wondering: Are we overbuilding like we did right before the 2008 housing crash?

No matter what you may hear in the news, there’s no reason for alarm. In reality, data shows builders aren’t racing ahead, they’re actually starting to tap the brakes.

Builders Are Pulling Back, Not Piling On

Permits (applications to start building new homes) are one of the best early indicators for what’s next for home construction. And right now, building permits are trending down, not up. Here’s why that’s so important.

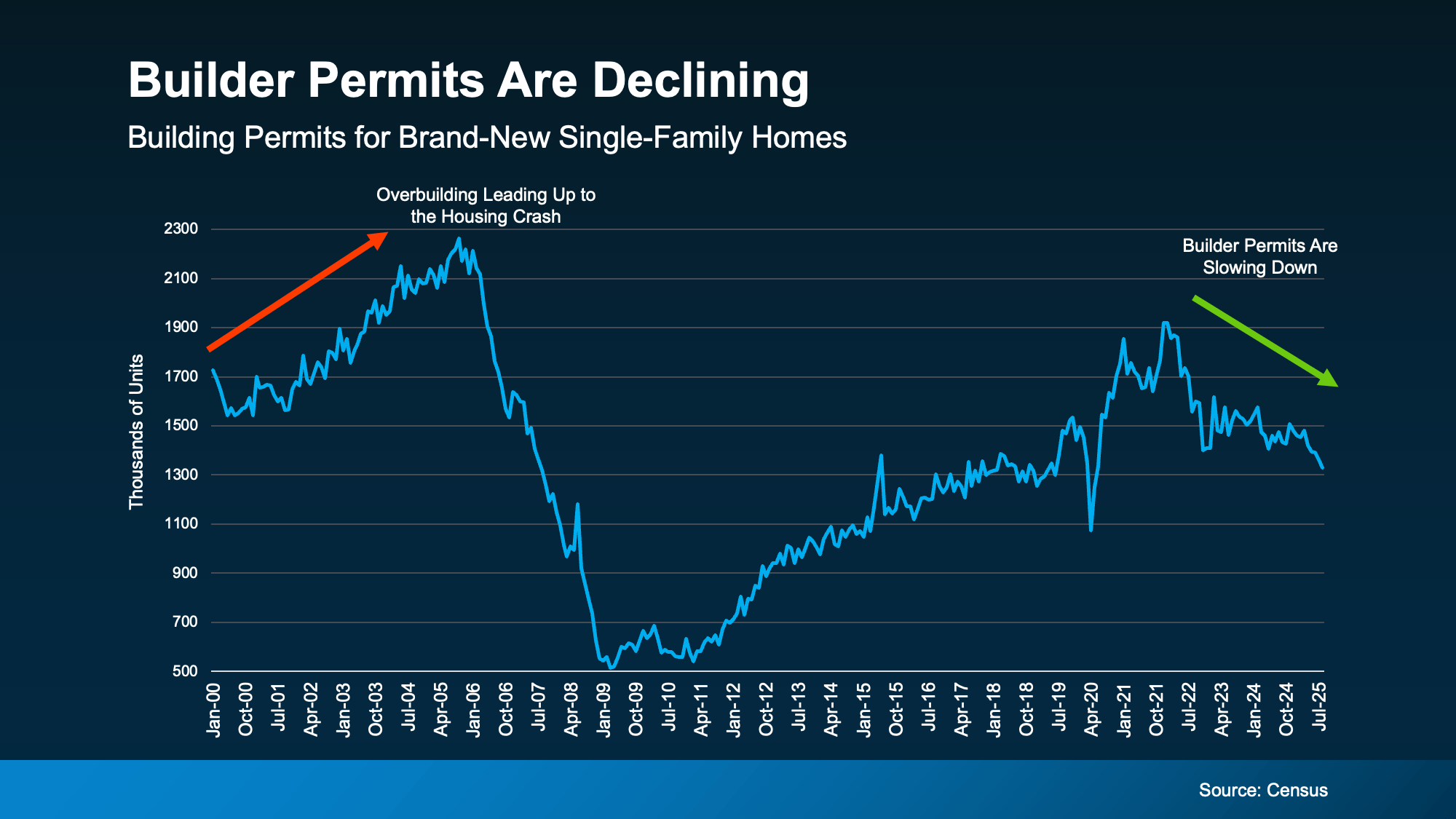

In the years before the housing crash of 2008, builders really ramped up their production of single-family homes (the red arrow in the graph below). And unfortunately, they built far more homes than the market actually needed. That oversupply led to falling home prices. That’s what so many people remember, and what they worry will happen again.

But while construction has been picking back up since roughly 2012, we’re not headed for a repeat of the same mistakes. The latest data available shows builders are actually starting construction on fewer homes right now (the green arrow in the graph below):

New data from the National Association of Home Builders (NAHB) confirms that trend. It shows that single-family building permits have fallen for eight straight months.

New data from the National Association of Home Builders (NAHB) confirms that trend. It shows that single-family building permits have fallen for eight straight months.

The Slowdown Isn’t Random, It’s Intentional

Basically, builders are watching and reacting to today’s economic conditions and buyer demand in real time. And they’re pumping the brakes on their pipelines to avoid getting caught with too much unsold inventory. As Ali Wolf, Chief Economist at Zonda, says:

“. . . builders are still working through their backlog of inventory but are more cautious with new starts.”

That’s a big contrast to what happened before the housing crash, when overconfidence led to record-breaking levels of new home construction – even as demand was dropping. Today’s builders aren’t overconfident. They’re listening to the market and adjusting before things get out of balance.

The Regional Picture Tells the Same Story

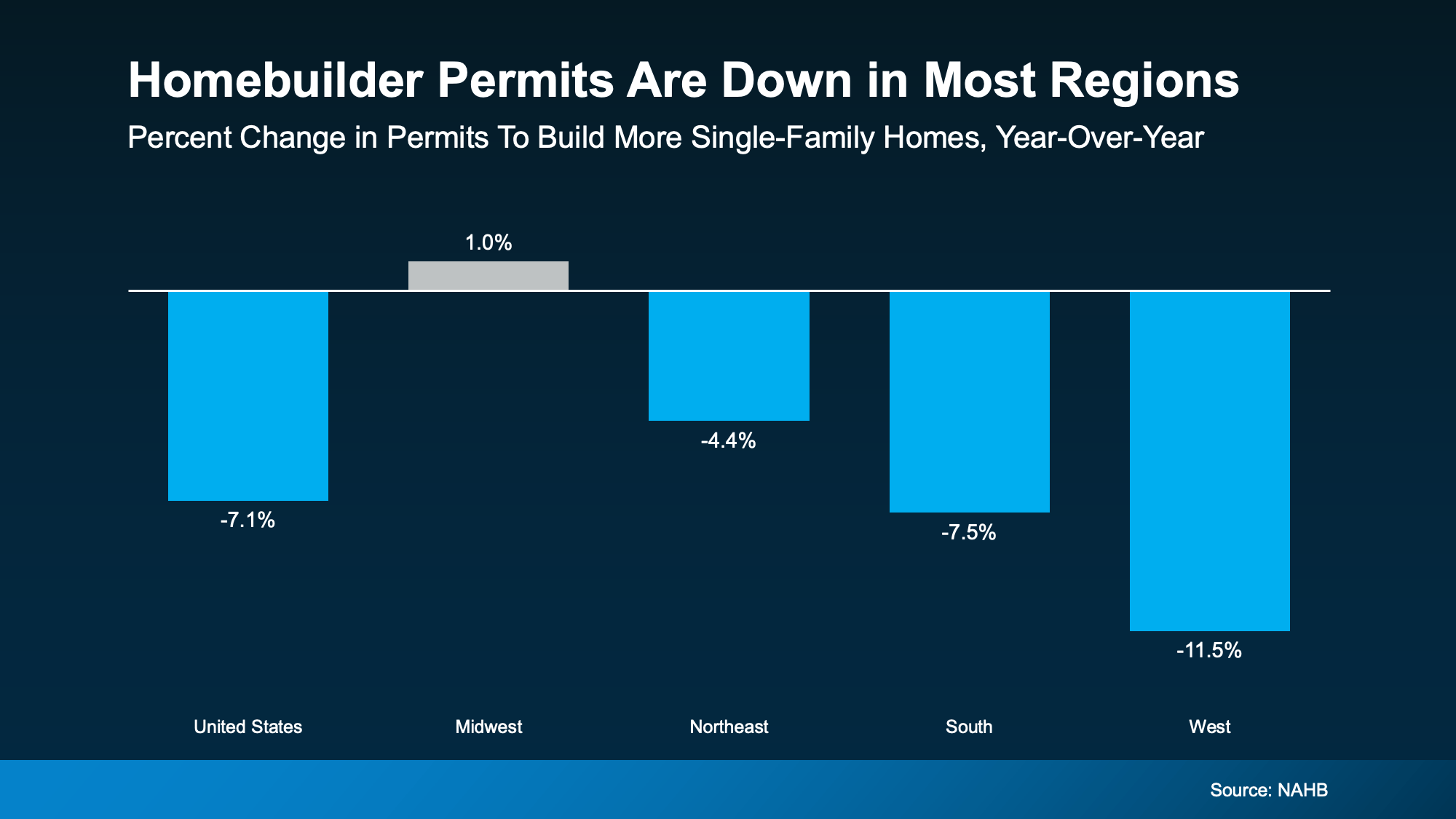

And while inventory is going to vary a lot based on where you live, if you zoom out and look at regional data, the pattern holds almost everywhere (see graph below):

NAHB reports single-family permits are down in nearly every part of the country, with just one region showing a slight uptick. And even there, the growth is so small, it’s practically flat.

NAHB reports single-family permits are down in nearly every part of the country, with just one region showing a slight uptick. And even there, the growth is so small, it’s practically flat.

Why This Isn’t 2008 All Over Again

In the lead up to the crash, builders kept building long after demand had disappeared. This time, they’re slowing down early, and that’s a good thing.

The market actually needs more homes after years of underbuilding. But builders are making sure they don’t have to overcorrect. They’re being intentional about how many homes they’re building right now.

So yes, you’re seeing more new homes for sale today, but that doesn’t mean we’re oversupplied nationally. It means buyers finally have more options, and builders are pacing themselves to keep things in check. They’re not going to flood the market. And that’s a really good thing for housing overall.

Bottom Line

Seeing more new homes for sale doesn’t mean builders are overdoing it. Since building permits have been declining for eight straight months, it’s clear this isn’t an out-of-control boom. It’s a measured recovery.

If you want to know more about what builders are doing in our area, let’s connect.

Buyer Advice and Aid •

November 10, 2025

The VA Home Loan Advantage: What Every Veteran Should Know Right Now

The VA Home Loan Advantage: What Every Veteran Should Know Right Now

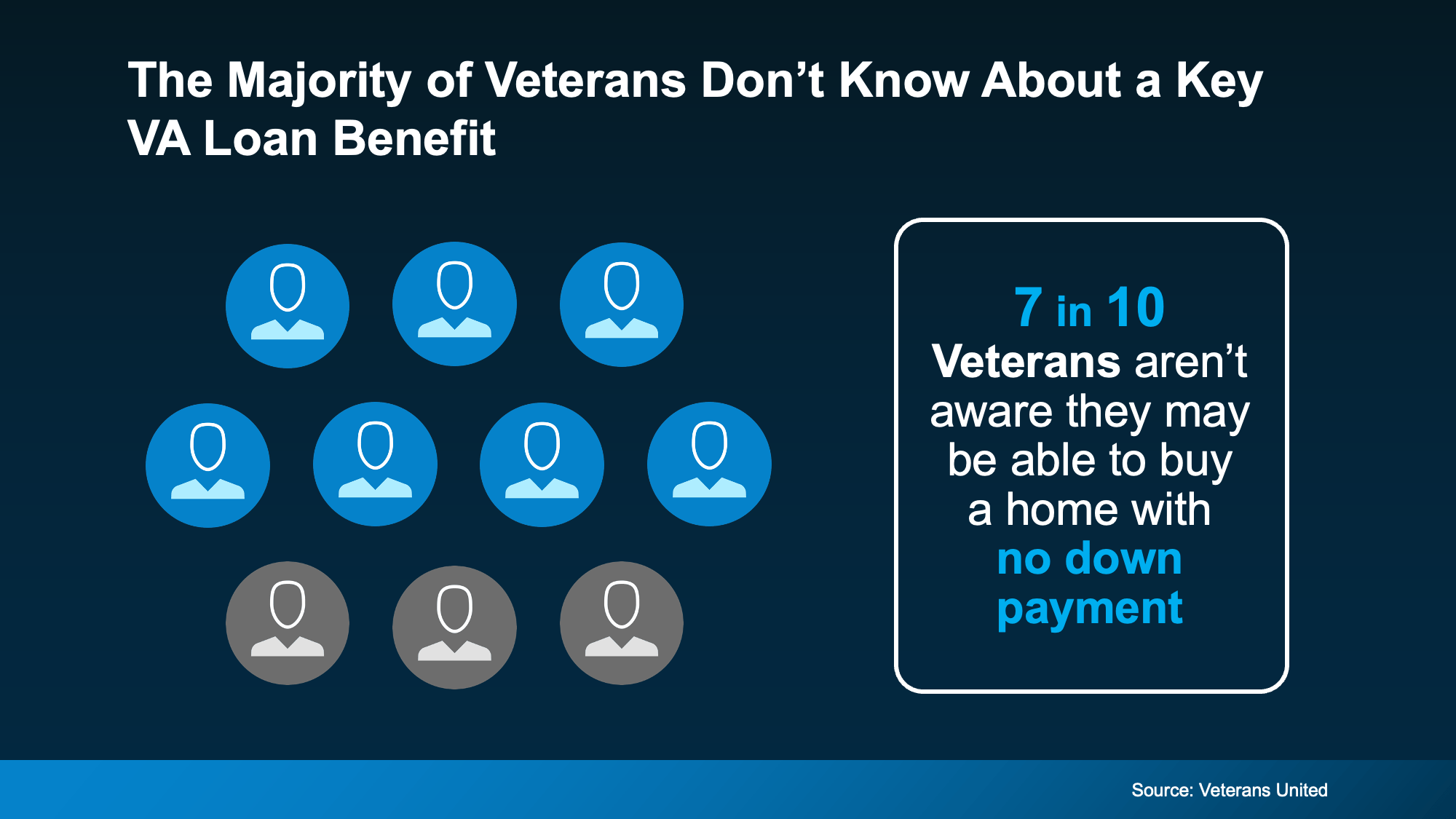

If you’ve served in the military (or if your spouse has), you have access to one of the most powerful homebuying tools out there. The chance to buy a home without having a down payment.

Unfortunately, 70% of Veterans (that’s 7 out of every 10) don’t know about this benefit, according to Veterans United.

And that’s a big missed opportunity for those who’ve earned this benefit through service. So, let’s break down what you really need to know about Veterans Affairs (VA) home loans right now.

And that’s a big missed opportunity for those who’ve earned this benefit through service. So, let’s break down what you really need to know about Veterans Affairs (VA) home loans right now.

Why VA Home Loans Can Be a Great Option

For nearly 80 years, VA loans have made homeownership possible for millions of Veterans and active-duty service members. Here are just a few of the top perks according to the Department of Veteran Affairs:

- Options for $0 Down Payment: Many Veterans can buy a home without spending years saving up.

- Fewer Upfront Costs: The VA limits which types of closing costs Veterans have to pay, helping you keep more cash on hand when you’re finalizing your purchase.

- No Private Mortgage Insurance (PMI): Unlike many other loan types, VA loans don’t require PMI, lowering your monthly costs.

These features make VA loans a great way for service members (or their family) to build stability, save money, and start creating long-term wealth through homeownership.

Can You Still Get a VA Loan with the Government Shutdown?

But lately, there’s been some confusion about whether VA loans are still available due to the government shutdown. And that uncertainty has kept some Veterans from taking the next step.

While there may be processing delays, Veterans United explains you can still get a loan:

“There’s been a lot of confusion and uncertainty about how a government shutdown will affect VA home loans . . . The good news is that the shutdown has minimal impacts on VA lending. Lenders are still able to order appraisals, obtain a borrower’s Certificate of Eligibility, submit the VA Funding Fee and more. In short, Veterans are still able to use their home loan benefit to buy a home or refinance an existing mortgage.”

So, despite the headlines, you can still use your VA home loan benefits today. The process is ready when you are. It just may take more time to go through.

Why the Right Agent and Lender Matter

Just remember, using your VA home loan is easier (and smoother) when you have the right team behind you. As VA News puts it:

“Choosing a military-friendly broker or agent who understands the VA home loan application process can make all the difference in the homebuying experience. Finding the right agency or brokerage is just as important as locking in a good VA mortgage lender. Communication is key to getting to the loan closing table.”

A knowledgeable agent and an experienced lender can help you navigate every step, all the way from qualifying to closing. With their help, you can make sure you’re getting the most out of your benefits.

Bottom Line

If you’re a Veteran, a VA home loan is one of the most valuable benefits you’ve earned through your service. It offers options for no down payment, limited closing costs, and more.

Want to learn more? Talk to a lender so you can take full advantage of the benefits you’ve earned.

Money & You •

November 6, 2025

What a Government Shutdown Really Means for the Housing Market

What a Government Shutdown Really Means for the Housing Market

There’s been a lot of talk lately about how a government shutdown impacts the housing market. You might be wondering: Is it causing everything to grind to a halt?

The short answer? No.

The housing market doesn’t stop. It keeps moving. Homes are still being bought and sold, contracts are still being signed, and closings are still happening. The difference is that a few parts of the process may slow down a little, but overall, the market continues to function.

Here’s What Typically Happens

Whenever the government shuts down, some federal agencies temporarily close or scale back their operations. That can cause a few hiccups in real estate, especially when it comes to processing certain types of government loans and insurance requirements:

- “Applicants for FHA, VA, or USDA loans—which account for about one-quarter of all mortgage applications—may encounter significant processing delays due to agency furloughs.” – Selma Hepp, Chief Economist at Cotality

- “By recent estimates, more than 2,500 mortgage originations per working day are at risk of delays during a shutdown . . .” – Zillow

- Flood insurance approvals may also be paused. The National Flood Insurance Program can be temporarily affected, which delays closings in flood zones.

Even with those challenges and delays, most transactions still go through. Buyers keep buying, sellers keep selling, and agents keep helping people move forward.

The Housing Market Usually Bounces Back Fast

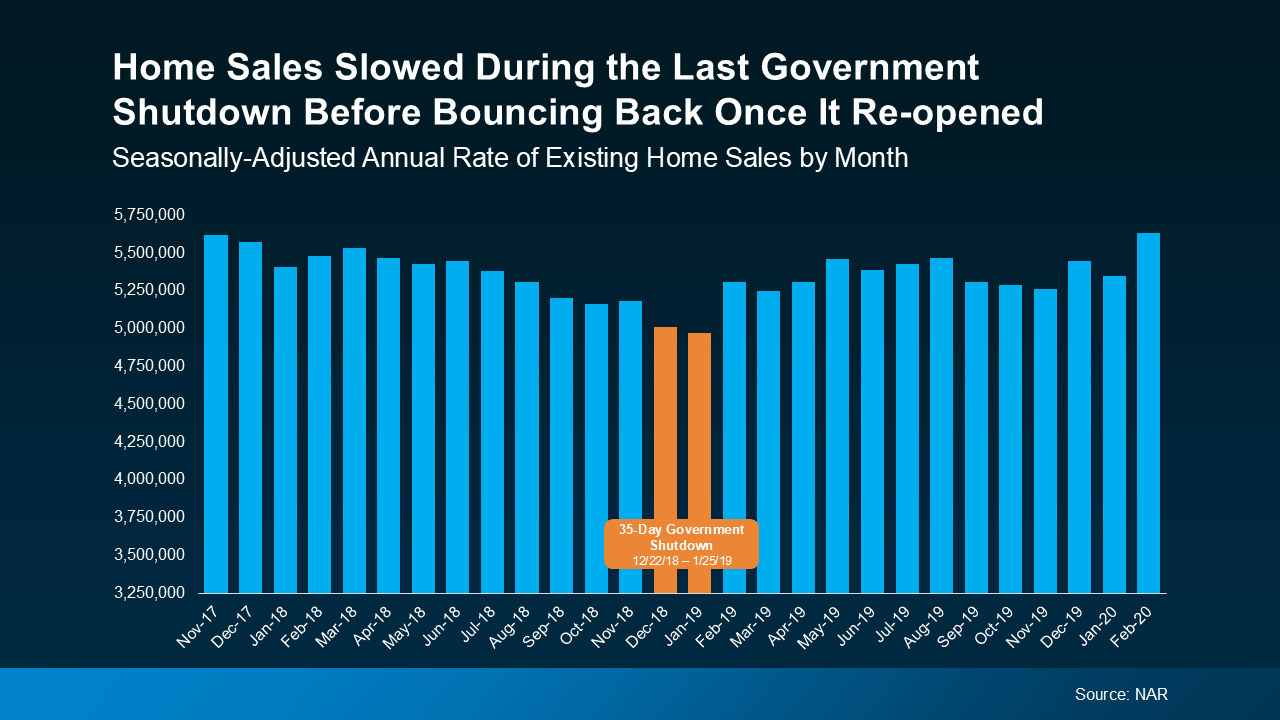

And you can see that play out in this data. If you look back at the most recent government shutdown that began at the end of 2018 and lasted for 35 days, sales activity dipped very slightly during the closure but picked right back up once the government reopened.

Data from the National Association of Realtors (NAR) shows existing home sales slowed for about two months, and then rebounded quickly as delayed closings worked their way through the system when the government reopened (see graph below):

What’s important to note is that the slowdown you see in the orange bars on this graph wasn’t simply due to seasonality in a typical housing market cycle. The sharper, shorter drop in this case lines up exactly with the 35-day government shutdown, and then sales bounced back as soon as it ended.

What’s important to note is that the slowdown you see in the orange bars on this graph wasn’t simply due to seasonality in a typical housing market cycle. The sharper, shorter drop in this case lines up exactly with the 35-day government shutdown, and then sales bounced back as soon as it ended.

What This Means for You

If you’re in the middle of buying or selling a home, don’t panic. Most deals will still move forward, even if it takes a few extra days. Jeff Ostrowski, Housing Market Analyst at Bankrate, explains:

“If you’re expecting to close in a week or a month, there could be some slight delay, but I think for most people, it’s probably going to be a blip more than a real deal killer.”

And if you’re just starting to think about buying or selling, this could actually work in your favor. Some buyers and sellers may become cautious and pause their plans during times of uncertainty, like this, and that can open a short window of opportunity.

When fewer people are active in the market, well-prepared buyers may find less competition for homes, and motivated sellers may be more willing to negotiate. These brief slowdowns often create a moment where you can make a move that would be harder once activity ramps back up.

Bottom Line

A government shutdown can cause short-term delays for some buyers, but it doesn’t derail the housing market. The last time this happened, sales picked back up as soon as the government re-opened.

If you’re unsure how this might affect your plans, or just want to make sense of what’s happening, let’s connect.

Homeowners •

November 5, 2025

Why Your Home Equity Still Puts You Way Ahead

Why Your Home Equity Still Puts You Way Ahead

If you’ve seen headlines about home prices dropping, it’s easy to wonder what that means for the value of your home too. Here’s what you really need to know.

Even with small price declines in some markets, data shows you’re likely still way ahead. And that’s thanks to your home equity.

The Relationship Between Home Prices and Equity

Home equity moves in sync with home prices. When prices rise, equity builds. When prices cool (even just slightly), equity growth does too. Here’s how that’s played out lately.

After the record-setting home price surge of 2020 and 2021, a little cooling was inevitable.

Back then, the number of homes for sale hit a record low. That caused home values (and your equity) to shoot up significantly as buyers fought over limited inventory.

But prices couldn’t continue to rise at that intense pace forever. The market had to moderate at some point, and that’s exactly what we’re seeing right now.

As more homes have come on the market this year, price growth slowed – so, equity gains did too. And that doesn’t mean you’ve lost ground.

Putting it into Perspective

You probably still have far more equity than you did just a few years ago. And that puts you in a strong position if you want to sell. Here’s the data to prove it.

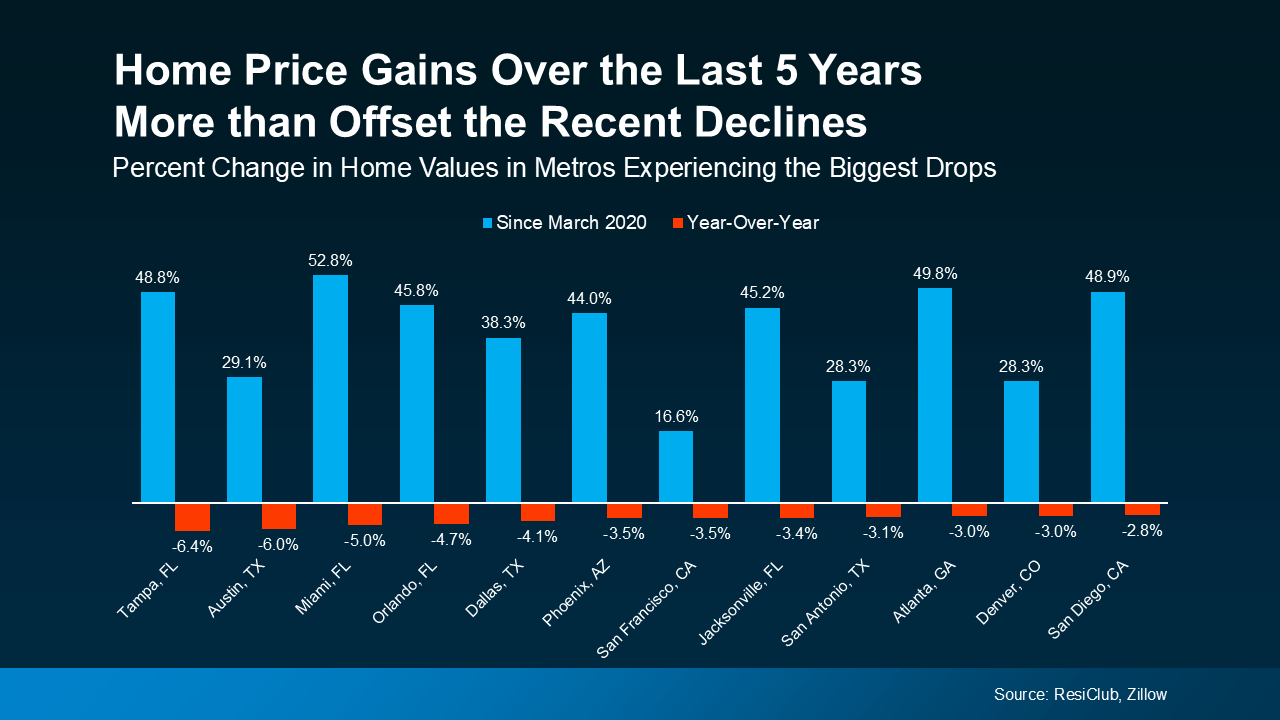

According to research from Zillow, home prices have risen a staggering 45% nationwide since March of 2020. That’s a big jump.

And in the majority of markets, prices are still rising, just at a much slower pace. But even in the metros where prices are experiencing the biggest declines (the ones making the headlines), the average drop is only about -4%.

So, what’s that really mean? In most places, prices are on the rise, so this isn’t even a concern. But in the few metros where prices are cooling off a bit, the 5-year gains more than offset those small dips.

In other words, these modest declines can’t erase years of growth. Homeowners who’ve been in their houses for several years are still way ahead. Big time. And that’s true pretty much everywhere.

In other words, these modest declines can’t erase years of growth. Homeowners who’ve been in their houses for several years are still way ahead. Big time. And that’s true pretty much everywhere.

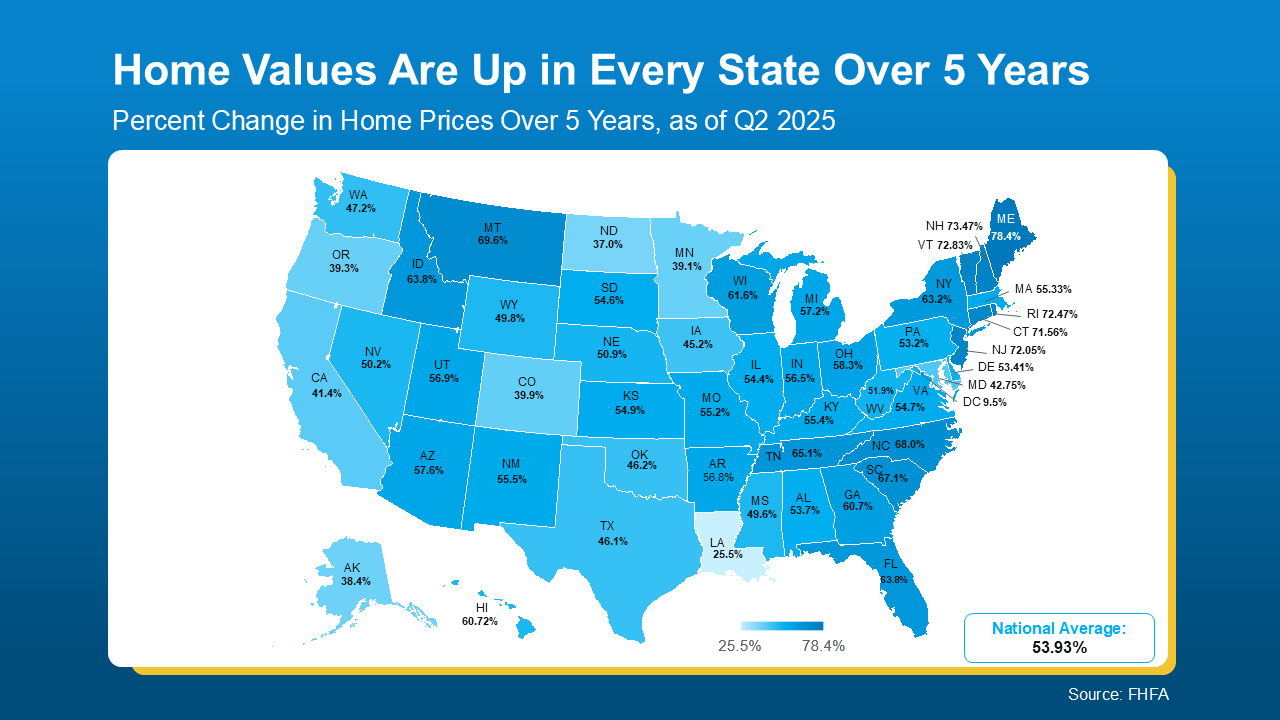

Data from the Federal Housing Finance Agency (FHFA) helps paint this picture. Let’s cast a slightly wider net and look at a state-by-state level this time. Every single state has seen prices go up over the last 5 years. And that means homeowners in each state have much more equity than they did just 5 years ago (see graph below):

Odds are, in most places, if you’ve owned your home for more than a few years, you’ve already built the kind of equity many people could only dream about before the pandemic. And if you sell, you can use it to help you downsize, or move up.

Odds are, in most places, if you’ve owned your home for more than a few years, you’ve already built the kind of equity many people could only dream about before the pandemic. And if you sell, you can use it to help you downsize, or move up.

And just in case you’re worried prices will crash and your equity will take a bigger hit in the near future, here’s what Jake Krimmel, Senior Economist at Realtor.com, has to say:

“The slight recent declines in aggregate value and total home equity are not cause for concern . . . Although the market is coming into better balance, large price declines nationally are extremely unlikely in the near term . . .”

The price moderation we’ve seen lately isn’t a cause for concern. It’s a signal of a market that’s finding its balance again after several years of unsustainable price growth. And after several years of major price appreciation, most homeowners are still in an incredibly strong position.

Bottom Line

Even with prices coming down in some markets, today’s homeowners are still sitting on near record amounts of equity.

If you’re wondering how much equity you have (or how far ahead you really are), let’s connect.

You might be surprised by what your home is actually worth today.

Buyer Advice and Aid •

October 29, 2025

Why You Don’t Need to Be Afraid of Today’s Mortgage Rates

Why You Don’t Need To Be Afraid of Today’s Mortgage Rates

Mortgage rates have been the monster under the bed for a while. Every time they tick up, people flinch and say, “Maybe I’ll wait.” But here’s the twist. Waiting for that perfect 5-point-something rate could end up haunting your wallet later.

The Magic Number

According to the National Association of Realtors (NAR):

“. . . a 30-year fixed rate mortgage of 6% would make the median-priced home affordable for about 5.5 million more households—including 1.6 million renters. If rates were to hit that magic number, it’s likely that about 10%—or 550,000—of those additional households would buy a home over the next 12 or 18 months.”

When the market hits that mortgage rate sweet spot, as expert forecasters are starting to say is more likely in 2026, the psychological shift to lower rates will kick in for more of today’s hopeful buyers. That will unleash some pent-up demand that’s been waiting on the sidelines, and the increase in activity will cause prices to rise.

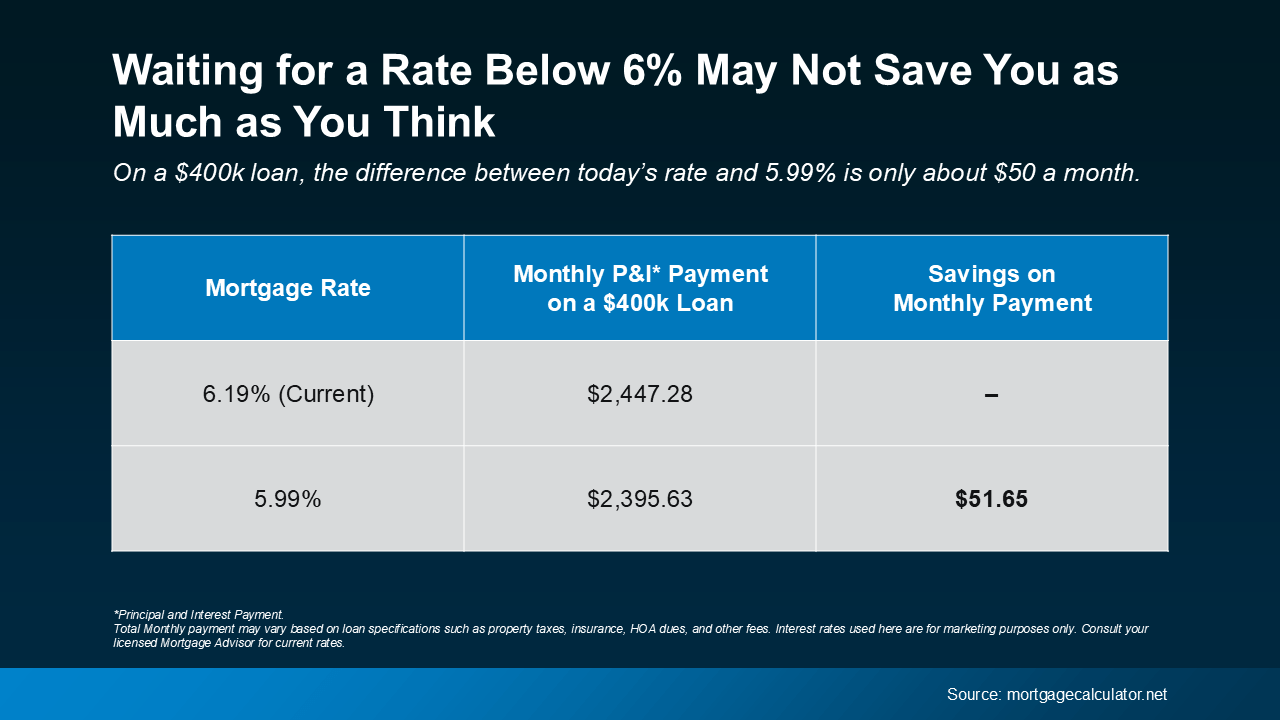

And while a 5.99% rate might sound like a big win, if you’re waiting for that number to make your move, it might not actually save you as much as you think. Here’s how the math looks when you run the numbers (see chart below):

On a $400,000 mortgage, the difference between today’s rate (around 6.2%) and 5.99% is roughly $50 a month. That’s less than many people spend on weekly coffee runs or occasional DoorDash orders. And as prices tick up with more buyers in the market, that could quickly negate any of your potential savings.

On a $400,000 mortgage, the difference between today’s rate (around 6.2%) and 5.99% is roughly $50 a month. That’s less than many people spend on weekly coffee runs or occasional DoorDash orders. And as prices tick up with more buyers in the market, that could quickly negate any of your potential savings.

So, if you’re waiting for 5.99%, that difference might not be worth missing out on today’s opportunities, like having more homes to choose from, better negotiation leverage with today’s sellers, and fewer buyers out there looking for the same houses.

Because the reality is, those benefits start to slip away when more buyers begin to make their moves – and a rate under 6% is exactly they’re waiting for.

Why Acting Now Makes Sense

Jessica Lautz, Deputy Chief Economist and VP of Research at NAR, says:

“Over the last 5 weeks, mortgage rates have averaged 6.31%. This has provided savvy buyers a sweet spot to reexamine the home search process with more inventory, widening their choices.”

And like Matt Vernon, Head of Retail Lending at Bank of America, notes:

“Rather than waiting it out for a rate that they like better, hopeful homebuyers should assess their personal financial situation—if the house is right for them, and the upfront and monthly payments are affordable, it could be the right chance to make a move.”

Bottom Line

If moving at today’s rate scares you, remember, waiting doesn’t always pay off. Once rates dip below 6%, as some experts project they’ll do next year, more buyers (and higher prices) will be back.

So, don’t be afraid of today’s mortgage rates. Because if you’re ready, this might just be your chance to make your move before the market wakes up again.

Seller Advice •

October 27, 2025

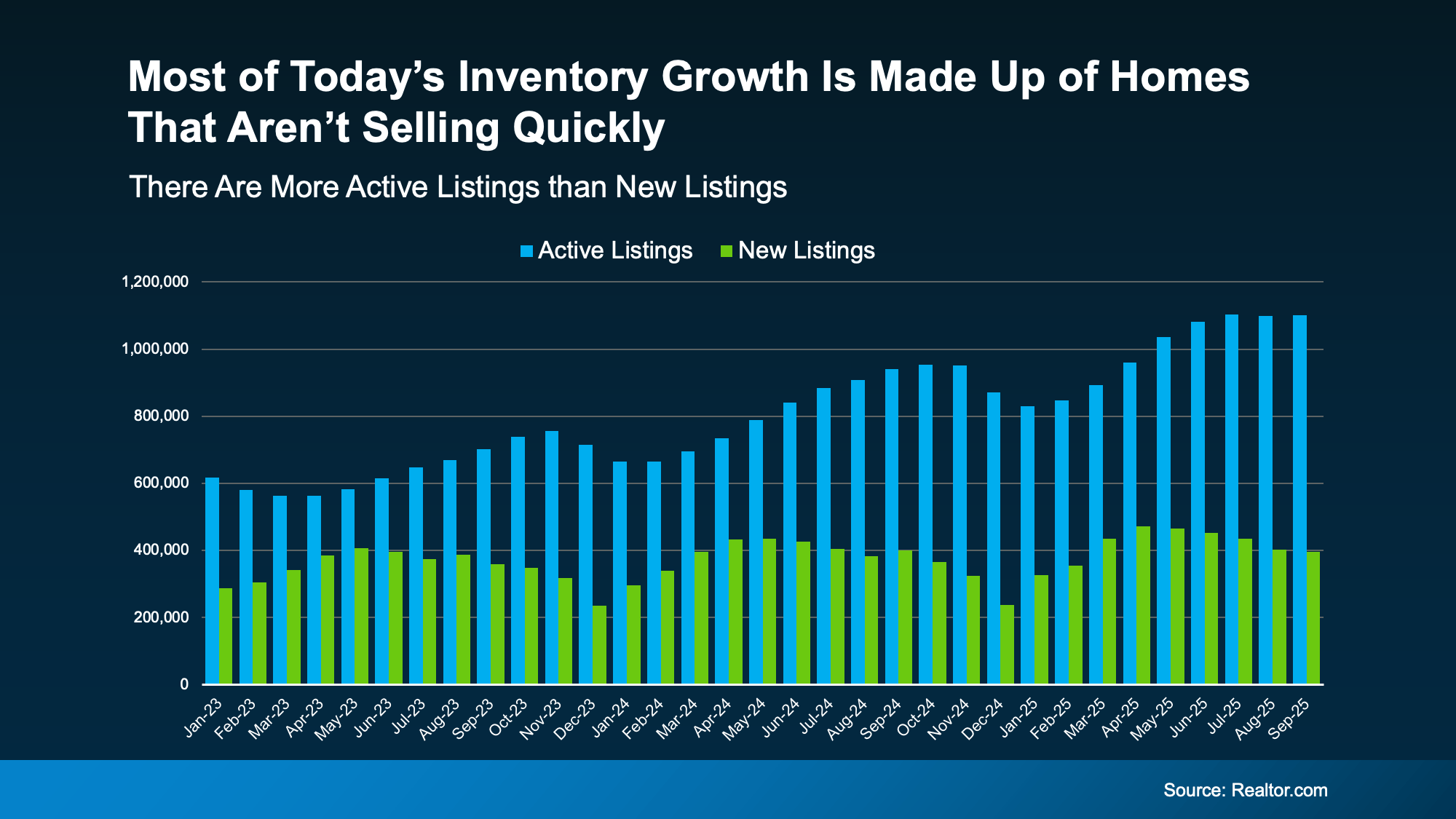

Why Some Homes Sell Quickly-and Others Don’t Sell at All

Why Some Homes Sell Quickly – and Others Don’t Sell at All

A few years ago, inventory hit a record low. Just about anything sold – and fast. But now, there are far more homes on the market. Listings are up almost 20% from this time last year. And in some areas, supply is even back to levels we last saw in 2017–2019. For sellers, that means one thing:

Your house needs to stand out and grab attention from day one.

That’s especially true when you consider why the number of homes for sale is up. Here’s how it works. Available inventory is a mix of:

- Active Listings: homes that have been sitting on the market, but haven’t sold yet

- New Listings: homes that were just put on the market

Data from Realtor.com shows most of the inventory growth lately is actually from active listings that are staying on the market and taking longer to sell (see the graph below).

The blue bars show active listings. These are the homes that are sitting month to month and not selling. The green bars are new listings, the homes that were just put on the market. And it’s clear there are fewer new listings compared to how many are staying on the market unsold.

Since you don’t want your house to be one of the ones that take a long time to sell, let’s break down where things can go sideways and how to set yourself up to sell quickly.

Since you don’t want your house to be one of the ones that take a long time to sell, let’s break down where things can go sideways and how to set yourself up to sell quickly.

Why Some Homes Sell and Others Sit

The secret to selling in today’s market is simple. Make sure your house is easy for buyers to say yes to as soon as it is listed.

Price it based on current conditions (not what your neighbor sold for 3 years ago). Make important repairs. And highlight the best things about your house. If you do that, it will sell in any market – sometimes even faster than you’d think. Because the truth is, homes that are priced right today are still selling.

It’s the homeowners who are clinging to outdated expectations that are seeing their house sit and their listing go stale. According to Redfin and HousingWire, here are some of the most common reasons sales stall out:

- Priced it too high from the start

- Skipped necessary repairs before listing

- Didn’t stage the house well

- Sellers won’t negotiate with buyers

- Limited availability for showings

- Ineffective marketing or listing pictures

Most of those things didn’t matter as much just a few years ago. When inventory was at a record low, sellers could skip the prep, name their price, and still walk away with multiple offers over their asking price.

But today’s market is different now that inventory has grown. And that means your approach needs to be different too.

You don’t want to try out old strategies and aim too high just to see what sticks. Your first few weeks on the market are everything. That’s when your listing gets the most attention – and when pricing or presentation mistakes hurt the most. Get it wrong up front and your house will sit…and sit. Get it right, and it’ll be snatched up before you know it.

The Right Agent Helps Your House Stand Out

Selling quickly isn’t about luck. It’s about knowing how to play to the market you’re in. And that’s where your agent comes in.

A great agent will analyze your local market, suggest a price based on the latest comparables sold in your neighborhood, and create a marketing plan that makes buyers pay attention from day one. They’ll also walk you through any repairs you need to make or whether you need to bring in a staging company. As the National Association of Realtors (NAR) explains:

“Home sellers without an agent are nearly twice as likely to say they didn’t accept an offer for at least three months; 53% of sellers who used an agent say they accepted an offer within a month of listing their home.”

That’s the power of getting it right (and getting expert help) from the start.

Bottom Line

There are more homes for sale today than there were even just a year ago, but that doesn’t have to work against you.

When your house is priced right, shows well, and is marketed effectively, it will sell. Let’s connect if you want to know how to make that happen in our market this fall.