Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Buyer Advice and Aid •

September 29, 2025

Closing Costs Unpacked: State by State Breakdowns for Today’s Buyers

Closing Costs Unpacked: State-by-State Breakdowns for Today’s Buyers

If you’re planning to buy a home this year, there’s one expense you can’t afford to overlook: closing costs.

Almost every buyer knows they exist, but not that many know exactly what they cover, or how different they can be based on where you’re buying. So, let’s break them down.

What Are Closing Costs?

Your closing costs are the additional fees and payments you make when finalizing your home purchase. Every buyer has them. According to Freddie Mac, they typically include things like homeowner insurance and title insurance, as well as various fees for your:

- Loan application

- Credit report

- Loan origination

- Home appraisal

- Home inspection

- Property survey

- Attorney

National vs. Local: Why the Numbers Look So Different

When you search for information about closing costs online, you’ll often see a national range, usually 2% to 5% of the home’s purchase price. While that’s a useful starting point if you’re working on your homebuying budget, it doesn’t tell the whole story. In reality, your closing costs will also vary based on:

- Taxes and fees where you live (like transfer taxes and recording fees)

- Service costs for things like title and attorney work in your local area

While the home price is obviously going to matter, state laws, tax rates, and even the going costs for title and attorney services can change what you expect to pay. That’s why it’s important to talk to the pros ahead of time so you know what to budget for. It can put you in control before you even start shopping.

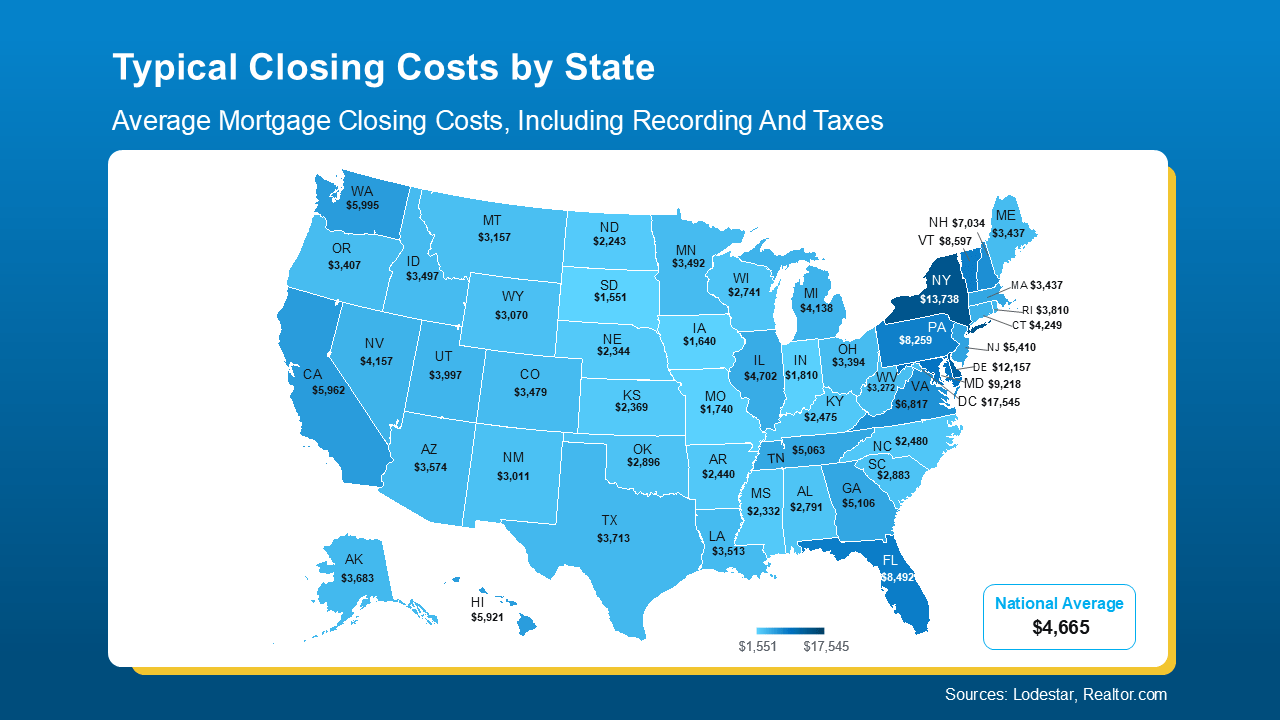

To give you a rough ballpark, here’s a state-by-state look at typical closing costs right now based on those factors for the median-priced home in each state (see map below):

As the map shows, in some states, typical closing costs are just roughly $1-3K. In a few places, they can be closer to $10-15K. That’s a big swing, especially if you’re buying your first home. And that’s why knowing what to expect matters.

As the map shows, in some states, typical closing costs are just roughly $1-3K. In a few places, they can be closer to $10-15K. That’s a big swing, especially if you’re buying your first home. And that’s why knowing what to expect matters.

If you want a real number to help with your budget, your best bet is to talk to a local agent and a lender. They can run the math for your price range, loan type, and exact location.

And just in case you’re looking at your state’s number and wondering if there’s any way to trim that bill, NerdWallet shares a few strategies that can help:

- Negotiate with the seller. Ask for concessions like a credit toward your closing costs.

- Shop around for homeowner’s insurance. Compare coverage and rates before you commit.

- Check for assistance programs. Some states, professions, and neighborhoods offer help. Your agent and lender can point you to what’s available locally.

Bottom Line

Closing costs are a key part of buying a home, but they can vary more than most people realize. Knowing your numbers (and how to potentially bring them down) can go a long way and help you feel confident about your purchase.

Let’s look at typical closing costs in our area and get you a personalized estimate, so you can craft your ideal budget.

Buyer Advice and Aid •

September 25, 2025

Downsizing Without Debt: How More Homeowners Are Buying Their Next House in Cash

Downsizing Without Debt: How More Homeowners Are Buying Their Next House in Cash

If you’ve been thinking about downsizing to lower your expenses, be closer to family, or just make life easier, here’s a trend worth paying attention to:

More homeowners are buying their next house outright, without taking on a new mortgage. And, if you’ve owned your home for a while, you may be able to do the same. No mortgage. No monthly housing payments.

A Record Share of Homeowners Are Mortgage-Free

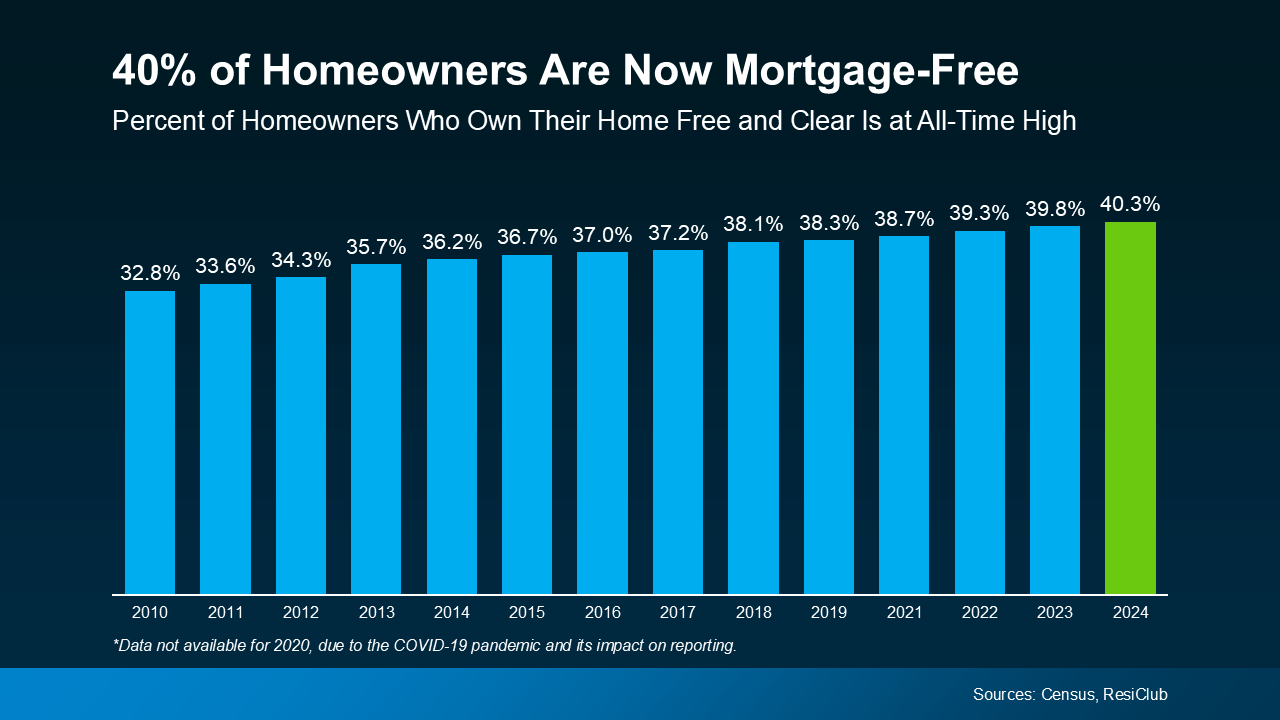

According to analysis from ResiClub of Census data, more than 40% of U.S. owner-occupied homes are mortgage-free – an all-time high for this data series. That means 4 in 10 homeowners own their homes free and clear (see graph below):

One big reason for this trend? Demographics. As Baby Boomers age and stay in their homes longer, many have had the time to fully pay off their mortgages. You might be in that group too and not even realize just how much buying power you now have. It’s time to change that.

One big reason for this trend? Demographics. As Baby Boomers age and stay in their homes longer, many have had the time to fully pay off their mortgages. You might be in that group too and not even realize just how much buying power you now have. It’s time to change that.

How Downsizers Are Turning Equity into Buying Power

As a homeowner, your equity is your biggest advantage in today’s market. If you’re mortgage-free (or close to it), it could give you the power to buy your next home in cash. That means you’d still have no mortgage payment in retirement, plus:

- Less financial stress as you age

- More cash flow, if you purchase a less expensive home

- And it would likely be a faster, simpler transaction

Here’s how it works. You’d sell your current house and use the proceeds to buy your next house in cash. And while that may sound like something you thought would never be possible for you, it’s more realistic than you may think.

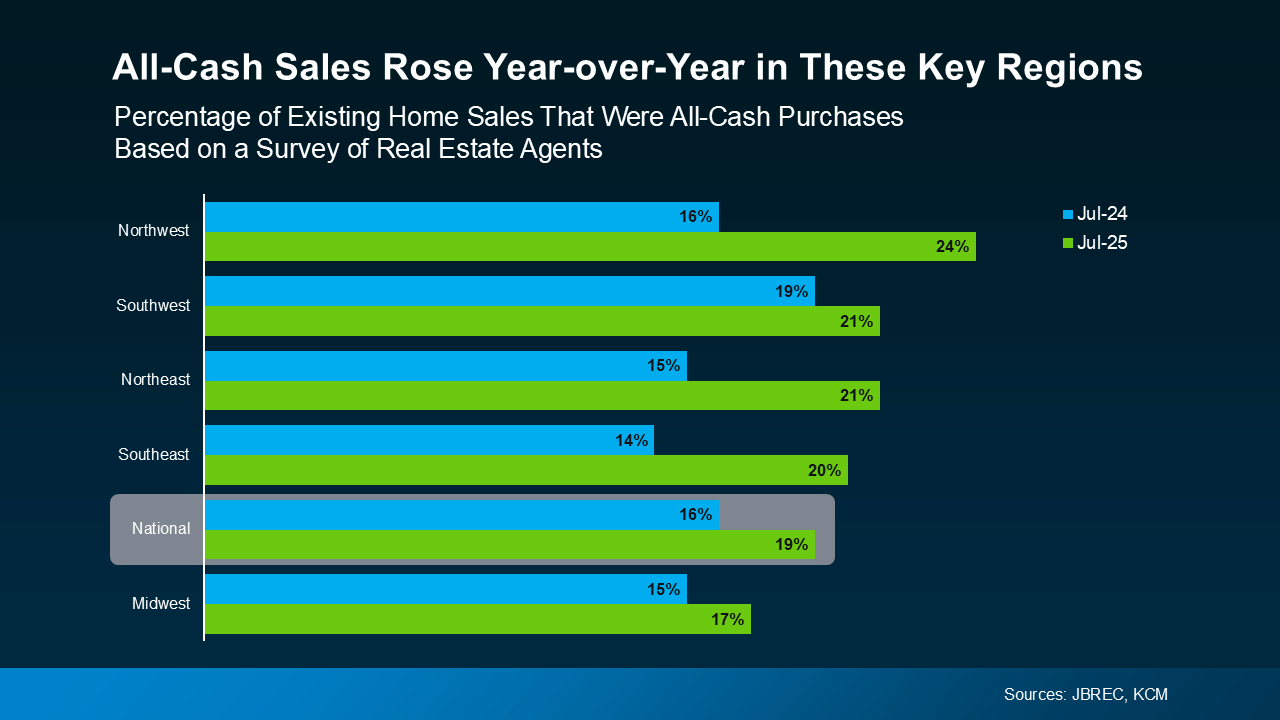

In the latest survey from John Burns Research and Consulting (JBREC) and Keeping Current Matters (KCM), agents reported the share of purchases with all-cash buyers is climbing nationally. And those agents are seeing increases in almost every region of the country (see graph below):

For Baby Boomers especially, buying in cash gives you more control over your next chapter. You could buy a smaller, less expensive home and have lower costs, less upkeep, and more flexibility to enjoy what matters most. All while staying debt and stress free.

For Baby Boomers especially, buying in cash gives you more control over your next chapter. You could buy a smaller, less expensive home and have lower costs, less upkeep, and more flexibility to enjoy what matters most. All while staying debt and stress free.

Because downsizing isn’t about downgrading your home. It’s about upgrading your quality of life. And that’s something worth exploring.

Bottom Line

You’ve worked hard for your home. Now it might be time for it to work hard for you.

Let’s talk about what your house is worth, and what it could unlock for you today. What would your ideal home look like if you were to downsize right now?

Buyer Advice and Aid •

September 22, 2025

3 Reasons Affordability Is Showing Signs of Improvement This Fall

3 Reasons Affordability Is Showing Signs of Improvement This Fall

For the past couple of years, it’s been tough for a lot of homebuyers to make the numbers work. Home prices shot up. Mortgage rates too. And a number of people hit pause because it just didn’t feel possible. Maybe you were one of them.

But there’s some encouraging news. If you’ve been waiting for a better time to jump back in, affordability may finally be showing signs of improvement this fall.

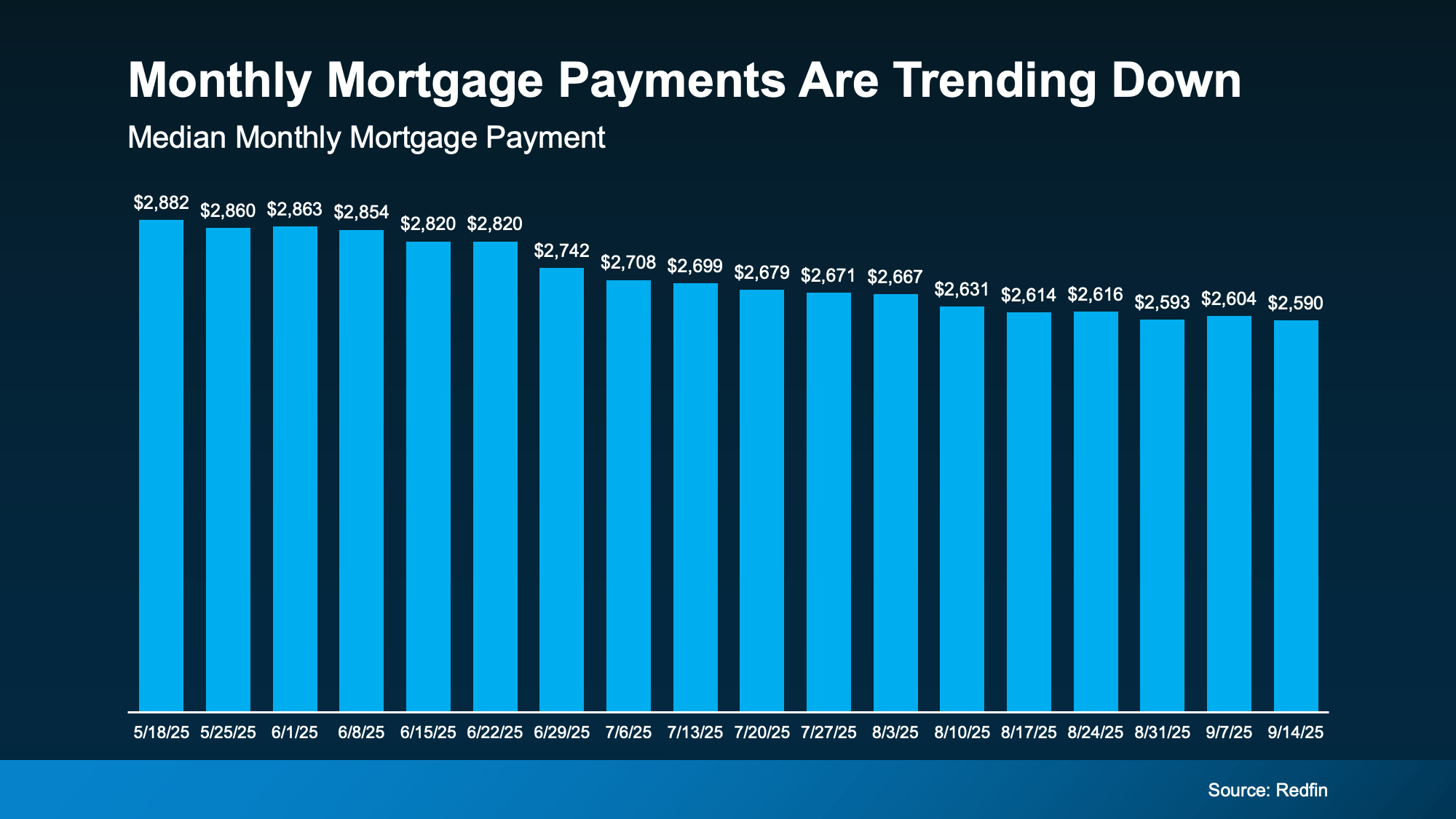

The latest data from Redfin shows the typical monthly mortgage payment has been coming down, and is now about $290 lower than it was just a few months ago (see graph below):

And here’s why this is happening. The cost of buying a home really comes down to three things:

And here’s why this is happening. The cost of buying a home really comes down to three things:

- Mortgage rates

- Home prices

- Your wages

Right now, all three are finally moving in a better direction for you. While that doesn’t mean it’s suddenly easy to buy at today’s rates and prices, it does mean it’s not as challenging.

1. Mortgage Rates

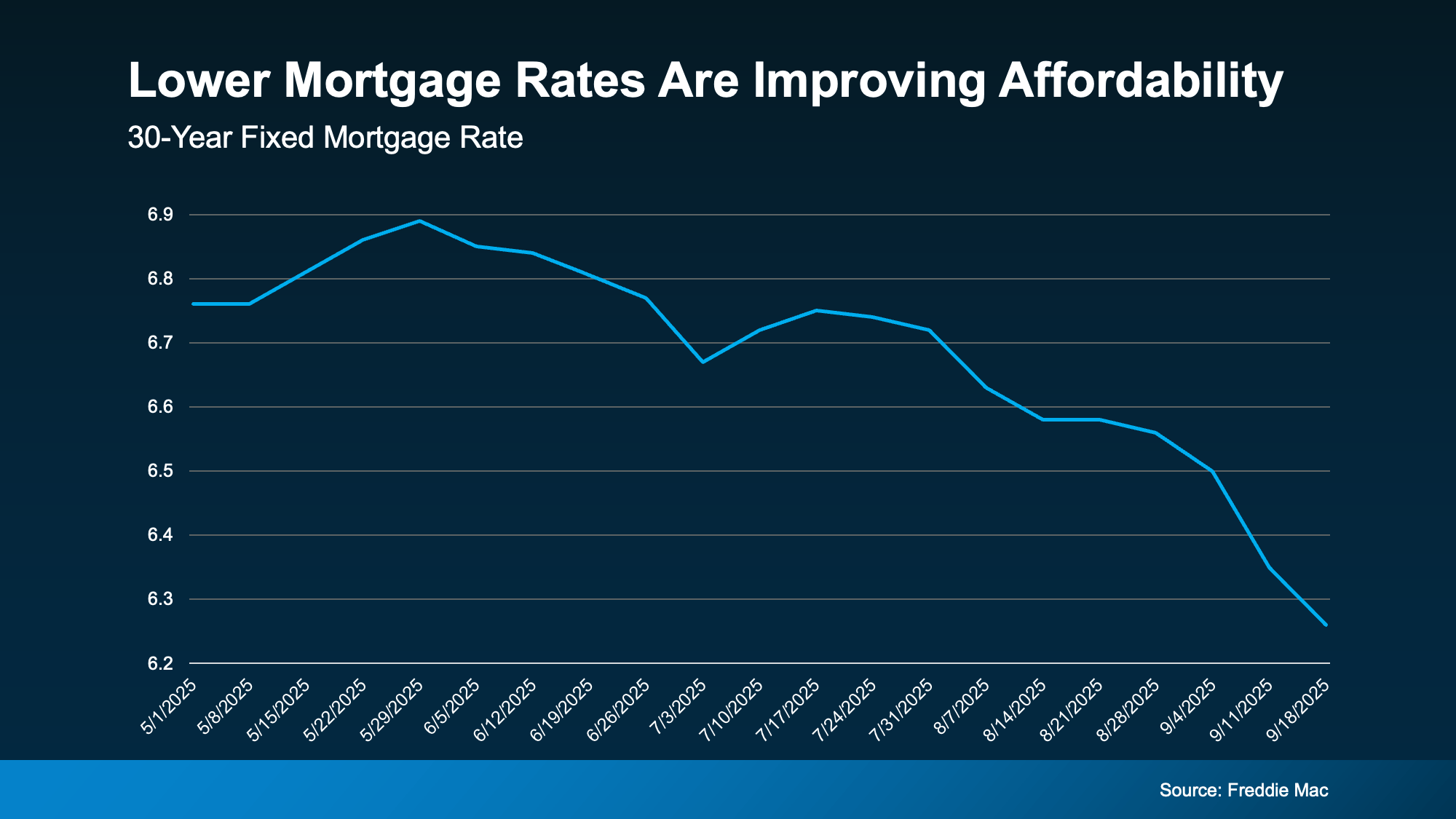

Mortgage rates have come down compared to earlier this year. In May, they were roughly 7%. And now, they’re closer to 6.3% (see graph below):

That may not sound like a big deal, but it does matter. Even small changes in rates can make a difference in your future monthly payment. Compared to when rates were 7%, if you take out an average $400K mortgage now at 6.3%, it’ll cost about $190 less a month based on just rates alone.

That may not sound like a big deal, but it does matter. Even small changes in rates can make a difference in your future monthly payment. Compared to when rates were 7%, if you take out an average $400K mortgage now at 6.3%, it’ll cost about $190 less a month based on just rates alone.

And for some people, that’s been enough to make buying a home possible again. As Joel Kan, VP and Deputy Chief Economist at the Mortgage Bankers Association (MBA), explained on September 10th:

“The downward rate movement spurred the strongest week of borrower demand since 2022 . . . Purchase applications increased to the highest level since July and continued to run more than 20 percent ahead of last year’s pace.”

2. Home Prices

After several years of prices rising very rapidly, price growth has finally slowed. As Odeta Kushi, Deputy Chief Economist at First American, puts it:

“National home price growth remains positive, but muted — low single digits — and we expect this trend to continue in the second half of the year.”

For buyers, that’s actually a big relief. That moderation makes it easier to plan your budget. And in some markets, prices have even dipped slightly. If you’re in one of the markets, you may be able to find something that’s more affordable than you’d expect.

3. Wages

According to the Bureau of Labor Statistics (BLS), wages are up near 4% annually. Lawrence Yun, Chief Economist at NAR, explains why that number is so important right now:

“Wage growth is now comfortably outpacing home price growth, and buyers have more choices.”

In other words, the typical paycheck is rising faster than home prices right now, which helps make buying a little more affordable. Now, it’s not a big difference, but in a market like this, every bit counts.

What This Means for You

Lower rates, slower price growth, and stronger wages might be enough to make the numbers finally work for you this fall.

While affordability is still tight, it’s a little easier on your wallet to buy now than it was just few months ago. Remember, data from Redfin shows the typical monthly mortgage payment is already around $290 lower than it was earlier this year.

Bottom Line

Have you been wondering if it’s worth taking another look at buying?

Let’s run the numbers together. We can go over your budget, see what’s changed, and figure out if this fall is the time to turn window-shopping into key-turning.

Homeowners •

September 18, 2025

Do You Know How Much Your House Is Really Worth?

Do You Know How Much Your House Is Really Worth?

Want to know something important you probably don’t have a professional check for you nearly as often as you should? Spoiler alert: it’s the value of your home.

Because here’s the reality. Your house is likely the biggest financial asset you have. And if you’ve lived in it for a few years or more, chances are it’s been quietly building wealth for you in the background – even if you haven’t been keeping tabs on it.

You might be surprised by just how much it’s grown, even as the market has shifted over the past few months.

What Is Home Equity?

That hidden wealth in your home is called equity. It’s the difference between what your house is worth today and what you still owe on your mortgage. Your equity grows over time as home values rise and as you make your monthly payments. Here’s an example to help you really understand how the math works.

Let’s say your house is now worth $500,000, and you have $200,000 left to pay off on your loan. That means you have $300,000 in equity. And that’s right in line with what the typical homeowner has right now.

According to Cotality, the average homeowner with a mortgage has about $302,000 in equity.

Why You Probably Have More Than You Think

Here are the two main reasons homeowners like you have near record amounts of equity right now:

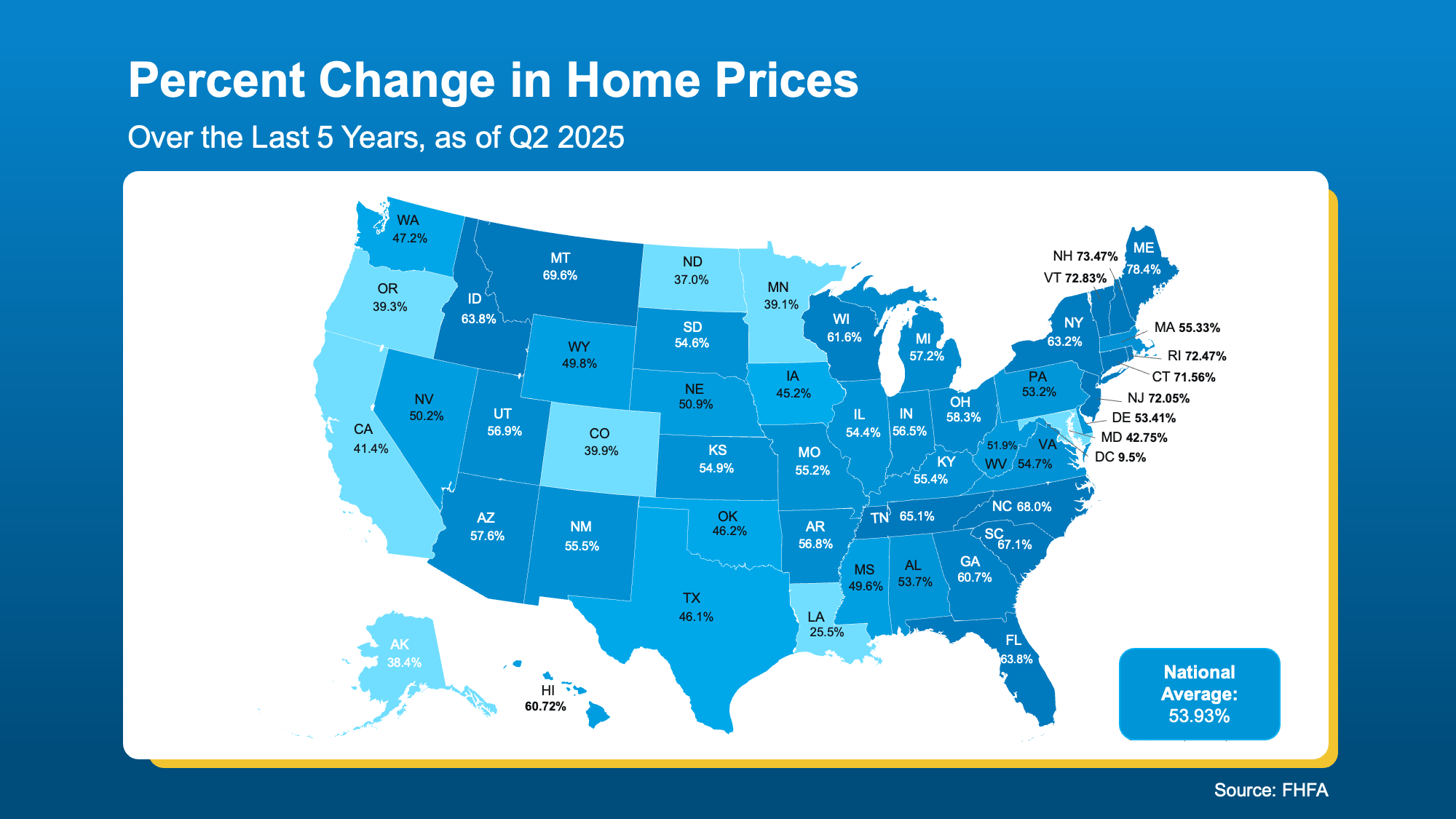

1. Significant Home Price Growth. According to the Federal Housing Finance Agency (FHFA), home prices have jumped by nearly 54% nationwide over the last five years (see map below):

This means your house is likely worth much more now than when you first bought it, thanks to how much prices have climbed over time. And if you’re worried because you’ve heard prices are flattening or even coming down in some markets, just know if you’ve been in your house for a few years (or more) you very likely have enough equity to sell and still come out ahead.

This means your house is likely worth much more now than when you first bought it, thanks to how much prices have climbed over time. And if you’re worried because you’ve heard prices are flattening or even coming down in some markets, just know if you’ve been in your house for a few years (or more) you very likely have enough equity to sell and still come out ahead.

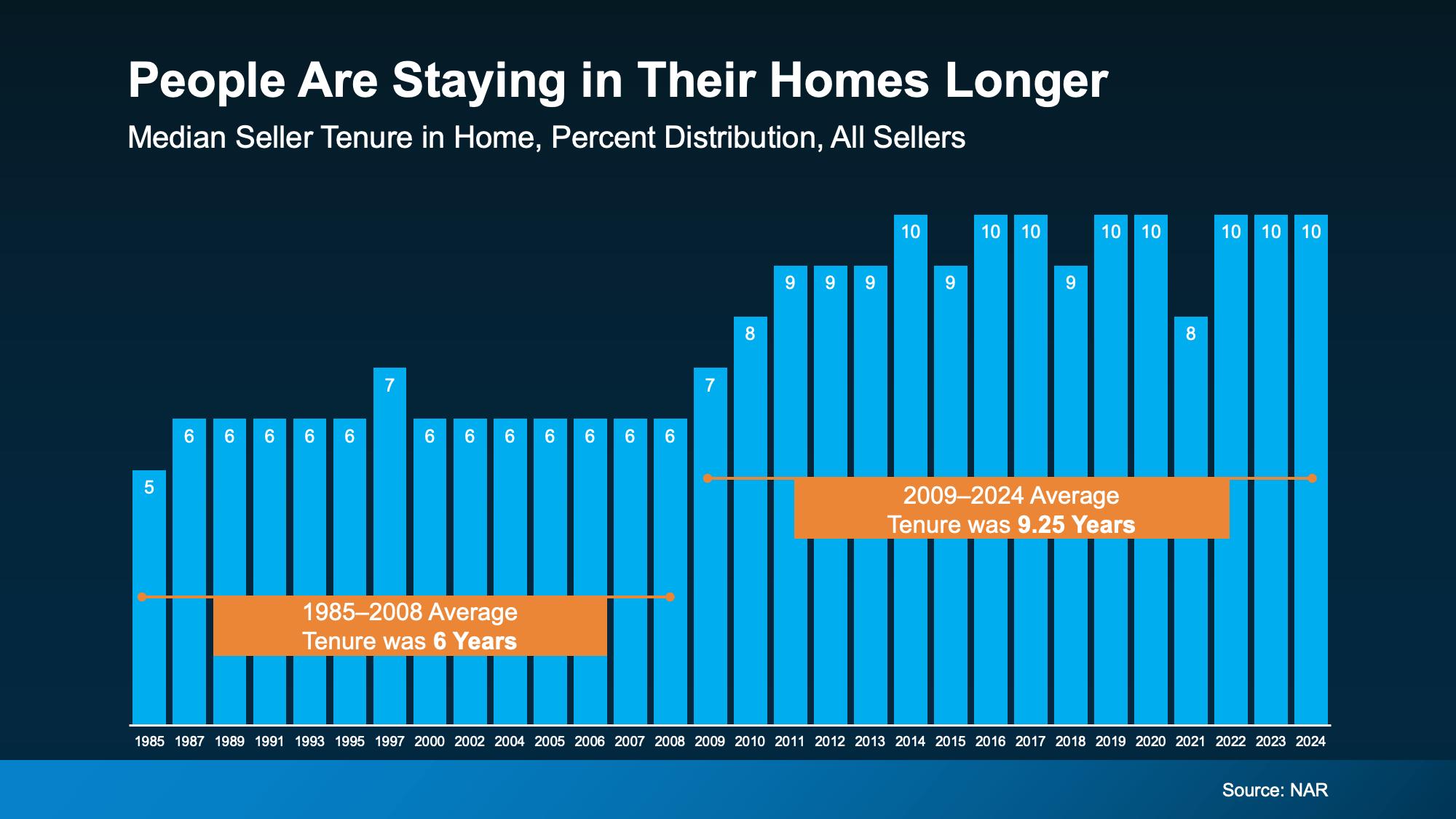

2. People Are Living in Their Homes Longer. Data from the National Association of Realtors (NAR), shows the average homeowner stays in their home for about 10 years now (see graph below):

That’s longer than it used to be. And over that decade? You’ve built equity just by making your mortgage payments and riding the wave of rising home values. Because the financial side of homeownership is about playing the long game, not worrying about little ups and downs in the market here and there. And over time, that means you’re winning.

That’s longer than it used to be. And over that decade? You’ve built equity just by making your mortgage payments and riding the wave of rising home values. Because the financial side of homeownership is about playing the long game, not worrying about little ups and downs in the market here and there. And over time, that means you’re winning.

So, if you’re one of those people who’s been in their home for a bit, here’s how much the behind-the-scenes price growth has helped you out. According to NAR:

“Over the past decade, the typical homeowner has accumulated $201,600 in wealth solely from price appreciation.”

What Could You Actually Do with That Equity?

Your equity isn’t just a number. It’s a tool you can use to unlock your next big move. Depending on your goals, you could:

- Use it to help buy your next home. Your equity could help you cover the down payment on your next home. In some cases, it might even mean you can buy your next house in all cash.

- Renovate your current house to better suit your life now. And, if you’re strategic about your projects, they could add even more value to your home if you do sell later on.

- Start the business you’ve always dreamed of. Your equity could be exactly what you need for startup costs, equipment, software, or marketing. And that could help increase your earning potential, so you’re getting yet another financial boost.

Bottom Line

Chances are, your house is worth quite a bit right now. If you’re curious about the value of your home, let’s connect. We’ll run the numbers and give you a professional equity assessment report, so you know what you’re working with and where you can go from here.

Seller Advice •

September 17, 2025

Why Now May Be a Key Moment To Sell Your House

Why Now May Be a Key 2025 Moment To Sell Your House

Mortgage rates are finally heading in the right direction – and buyers are starting to jump back in.

According to the data, buyer demand picked up considerably once mortgage rates hit a new low for 2025. The Mortgage Bankers Association (MBA) reports that applications for home loans were up 23% compared to the first week of September last year.

If you’ve been waiting to sell, or your listing recently expired because the market was slower than you hoped it would be, now’s the time to reconsider your move. Buyer demand is the highest it’s been since July – and you don’t want to miss this window.

When Rates Drop, Buyers React

Here’s what’s happening. The 30-year mortgage rate dropped to 6.13% earlier this week. And that’s the lowest it had been since October 2024. That decline followed weak job growth and other economic indicators that are fueling speculation the Federal Reserve may cut the Federal Funds Rate multiple times this year. Mortgage rates started dropping because financial markets are anticipating those Fed decisions. And that opens the door for more buyers to act.

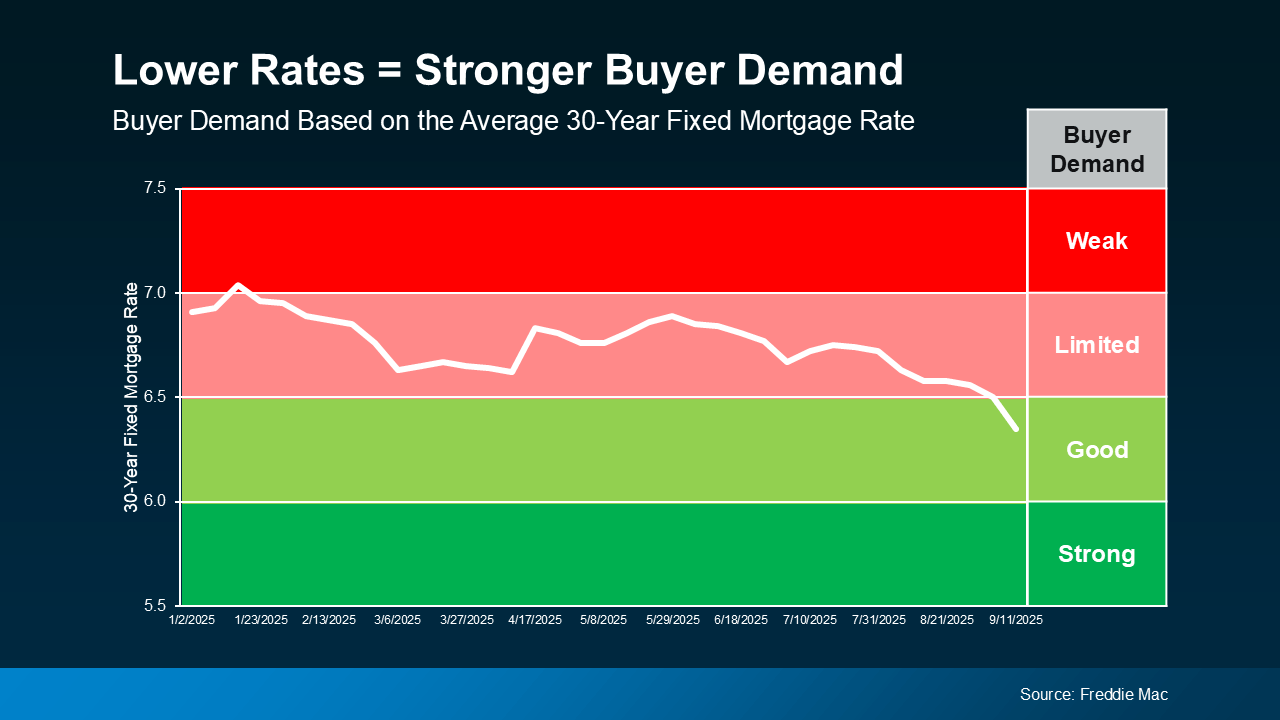

Since today’s buyers are looking at every angle to make home purchases more affordable, they’re much more sensitive to even the slightest movement in mortgage rates. Basically, it boils down to this. As affordability improves, so does buyer demand (see graph below):

And that’s a change you’re going to feel – in a good way. Since about this time last year, we’ve been in a plateau of “limited” buyer demand. But now that rates are coming down, buyer demand is getting better.

And that’s a change you’re going to feel – in a good way. Since about this time last year, we’ve been in a plateau of “limited” buyer demand. But now that rates are coming down, buyer demand is getting better.

What This Means for You

If you’re looking to move, it’s time to get serious about what’s happening in the market, and how you can use these key moments to your advantage. Maybe you have an expired listing that sat without offers earlier this year, or you held off on selling altogether, thinking buyers weren’t out there. This is your signal – they’re coming back. Now, it’s not in the big surge the market saw a few years ago, but this could be your window.

Here’s the opportunity. You can list, while buyer activity is rising and before more sellers in your neighborhood do too. Other homeowners may not see this shift for a while, so you can get a leg up on your competition if you act now.

On the flip side, if you wait, sure there may be more buyers if rates continue to inch down. But there are also going to be more sellers too. So, why take that risk?

A trusted local agent can help you assess your home’s value, fine-tune your pricing strategy, and make sure it stands out to the serious buyers who are taking action today.

Bottom Line

Buyers are watching rates, weighing their options, and starting to get off the sidelines. If you’re thinking about selling, this may be your chance to get ahead.

Want to make sure your house shows up for the right buyers, at the right time?

Let’s connect and walk through the steps together so you can make the most of this moment.

Real Estate Trends •

September 16, 2025

Only 2% of Home Sales are Foreclosures or Short Sales

Foreclosures aren’t flooding the market. Far from it.

Only 2% of home sales in July were foreclosures or short sales. That’s close to a record low.

And that’s a very different story than 2008 crash.

Want to know what’s happening in our area? Let’s connect.

#Foreclosures #HousingMarketUpdate #KeepingCurrentMatters

Uncategorized •

September 15, 2025

What a Fed Rate Cut Could Mean for Mortgage Rates

What a Fed Rate Cut Could Mean for Mortgage Rates

The Federal Reserve (the Fed) meets this week, and expectations are high that they’ll cut the Federal Funds Rate. But does that mean mortgage rates will drop? Let’s clear up the confusion.

The Fed Doesn’t Directly Set Mortgage Rates

Right now, all eyes are on the Fed. Most economists expect they’ll cut the Federal Funds Rate at their mid-September meeting to try to head off a potential recession.

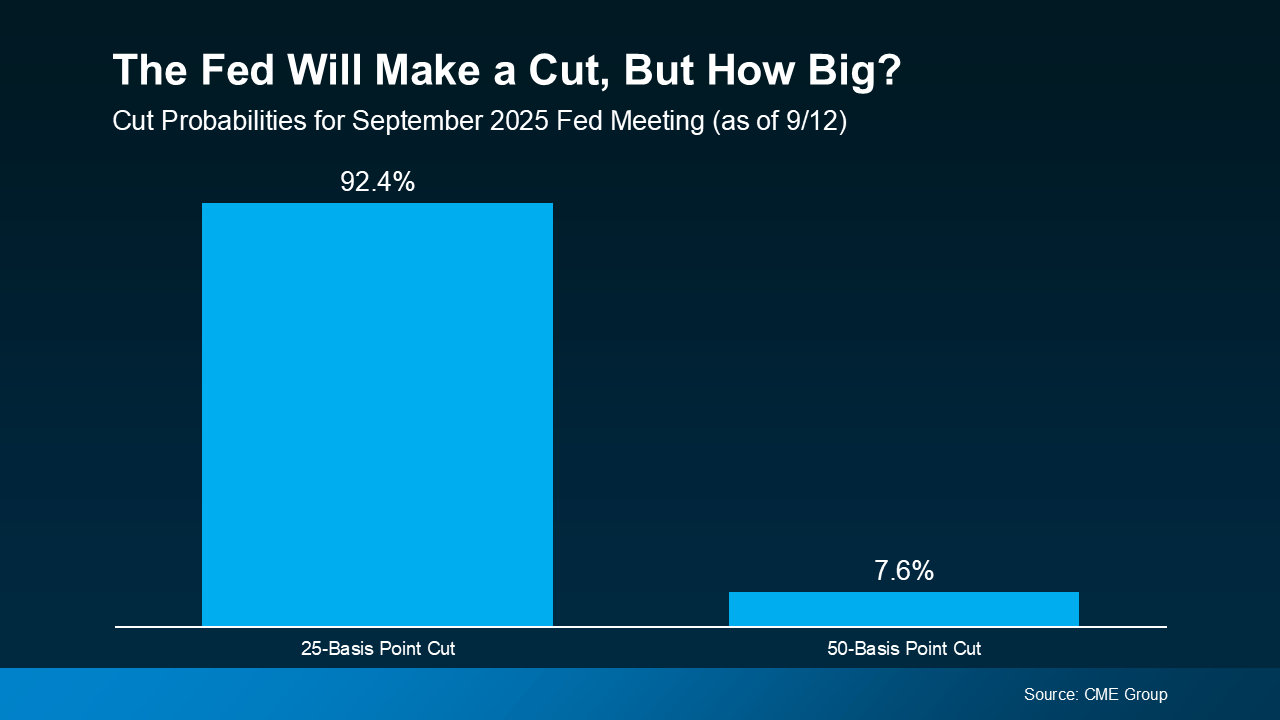

According to the CME FedWatch Tool, markets are already betting on it. There’s virtually a 100% chance of a September cut. And based on what we know now, there’s about a 92% chance it’ll be a small cut (25 basis points) and an 8% chance it will be a bigger cut (50 basis points):

So, what exactly is the Federal Funds Rate? It’s the short-term interest rate banks charge each other. It impacts borrowing costs across the economy, but it’s not the same thing as mortgage rates. Still, the Fed’s actions can shape the direction mortgage rates take next.

So, what exactly is the Federal Funds Rate? It’s the short-term interest rate banks charge each other. It impacts borrowing costs across the economy, but it’s not the same thing as mortgage rates. Still, the Fed’s actions can shape the direction mortgage rates take next.

Why Markets Already Saw This Cut Coming

Here’s the part that may surprise you. Mortgage rates tend to respond to what the financial markets think the Fed will do, before the Fed officially acts. Basically, when markets anticipate a Fed cut, that outlook gets priced into mortgage rates ahead of time.

That’s exactly what happened after weaker-than-expected jobs reports on August 1 and September 5. Each time, mortgage rates ticked down as financial markets grew more confident a cut was coming soon. And even though inflation rose slightly in the latest CPI report, the Fed is still expected to make a cut.

So, if the Fed goes with a 25-basis point cut, as expected, that’s likely already baked in to current mortgage rates, and we may not see a dramatic drop.

But if they go bigger and drop their Federal Funds Rate by 50 basis points instead, mortgage rates could come down more than they already have.

So, Where Do Mortgage Rates Go from Here?

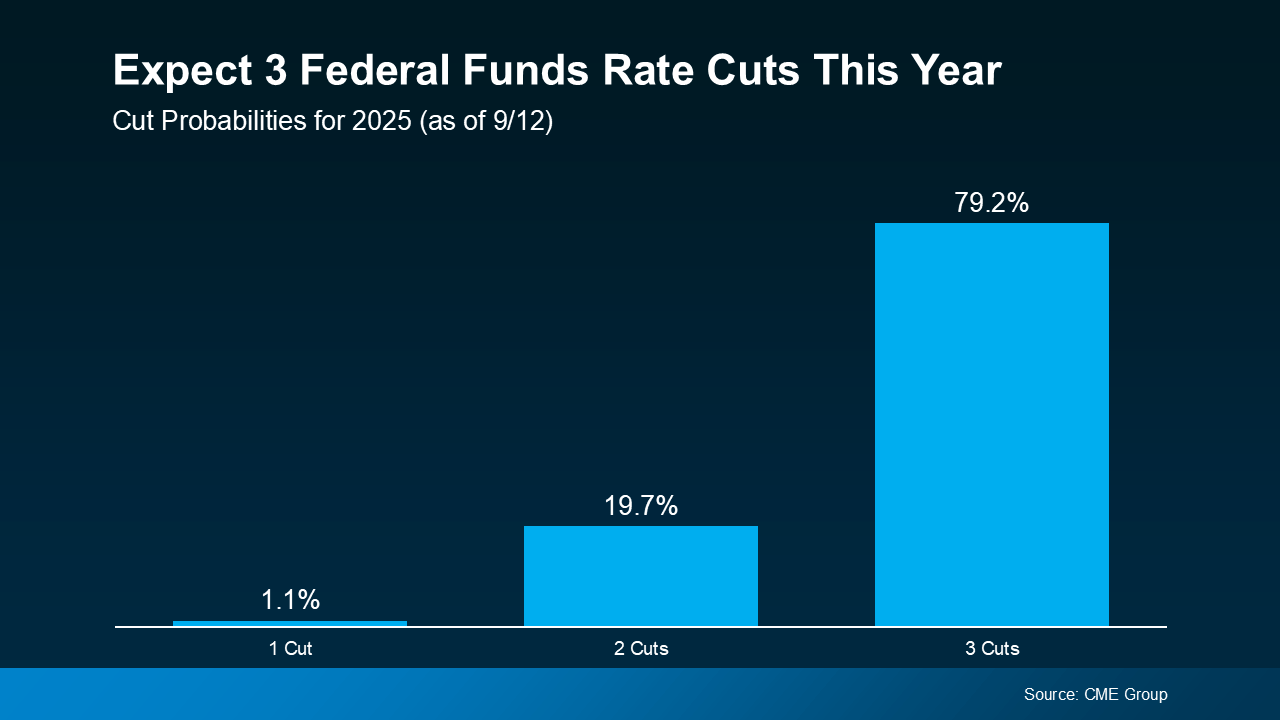

While the upcoming cut may not move the needle much, many experts expect the Fed could cut the Federal Funds Rate more than once before the end of the year. Of course, that’s if the economy continues to cool (see graph below):

As Sam Williamson, Senior Economist at First American, explains:

As Sam Williamson, Senior Economist at First American, explains:

“For mortgage rates, investor confidence in a forthcoming rate-cutting cycle could help push borrowing costs lower in the back half of 2025, offering some relief to housing affordability and potentially helping to boost buyer demand and overall market activity.”

If multiple rate cuts happen, or even if markets just believe they will, mortgage rates could ease further in the months ahead. But here’s the catch – all of this depends on how the economy evolves. Surprise inflation data or unexpected shifts could quickly change the outlook.

Bottom Line

Mortgage rates likely won’t drop sharply overnight, and they won’t mirror the Fed’s moves one-for-one. But if the Fed begins a rate-cutting cycle, and markets continue to expect it, mortgage rates could trend lower later this year and into 2026.

If you’ve been waiting and watching the housing market, now’s the time to talk strategy. Even small changes in rates can make a meaningful difference in affordability, and understanding what’s ahead helps you make the best decision for your situation.

Seller Advice •

September 11, 2025

Patience Won’t Sell Your House, Pricing Will

Patience Won’t Sell Your House. Pricing Will.

Waiting for the perfect buyer to fall in love with your house? In today’s market, that’s usually not what’s holding things up. And here’s why.

Let’s be real. Homes are taking a week longer to sell than they did a year ago. According to Realtor.com:

“Homes are also taking longer to sell. The typical home spent 60 days on the market in August, seven days longer than last year and now above pre-pandemic norms for the second consecutive month. This was the 17th straight month of year-over-year increases in time on market.”

Part of that is because there are more homes on the market. So, with more options for buyers to choose from, they aren’t getting snatched up quite as fast. But there’s another big reason: price.

The Average List Price Isn’t Going Up – and That Matters

Today, a lot of homeowners are overshooting their list price. They remember the big climb in home prices a few years ago, and they don’t realize how much has changed.

One of the most important, but often overlooked, changes in today’s housing market is this: average list prices have held steady for the past few years.

That’s a big shift from a typical market, where prices were rising steadily each year. And it’s significantly different than the 2021-2022 surge when sellers could set their price just about anywhere and still attract multiple offers over asking.

But now? That trend has leveled off – and sellers who want to stay competitive need to take note (see graph below):

Here’s what this says about today’s market. Buyers are a lot more price sensitive now. And sellers can’t keep trying to inch the bar higher, or their house will sit without any offers.

Here’s what this says about today’s market. Buyers are a lot more price sensitive now. And sellers can’t keep trying to inch the bar higher, or their house will sit without any offers.

Homeowners who expect to bring in more than their neighbors did last year may be setting themselves up for a longer, more frustrating experience.

And while homeowners are starting to realize prices can’t keep climbing at such a rapid pace, the hiccup is that list prices aren’t actually coming down yet as a result. They’re hanging around, holding steady. And sellers who make this mistake are often holding onto hope that they’ll be able to eek a few more dollars out of their sale. But that’s the problem right there.

If you want to sell today, you need to be in line with where the market is today. Not last year. Not during the pandemic. Today.

Because buyers will skip over homes that feel overpriced, even if it’s only by a little. It’s not that they aren’t interested. It’s just that in a market with more homes to choose from, buyers can be more selective, and sellers don’t get the same benefit of the doubt. If your house isn’t priced to sell, buyers just move on. They’ve got other options anyway.

4 Signs Your Price May Be Too High

You may already be feeling this yourself. If your home is listed and you’re not seeing results, watch for these common red flags noted by Bankrate:

- You’re not getting many showings

- You haven’t gotten any offers (or you’ve only gotten lowball offers)

- Buyers that do come to see your house leave overly negative feedback

- Your house has been sitting on the market longer than the average for your area

If any of these sound familiar, know that waiting it out won’t fix it. But adjusting your price will.

So, What’s the Solution?

Work with your agent to make sure your house is positioned for today’s market. Depending on your what’s happening in your local area, a few weeks without traction can raise questions for buyers about whether your price is realistic. And don’t worry – it doesn’t have to be a big drop. Even a small adjustment can be enough to bring the right buyers through the door.

And if you’re worried you won’t get the high-ticket sale price you thought you would be able to land, keep in mind that your equity has probably grown quite a bit. Chances are, you’re still ahead of the game simply because you invested in a home over the last 5, 10, or more years. You’re still winning when you sell today.

Bottom Line

Patience isn’t a strategy. Pricing is.

If your home isn’t moving, the market is telling you something – and the right price can change everything. Your house will sell, if you price it strategically.

Talk to your agent about what buyers are willing to pay right now to make sure your home stands out for all the right reasons.